Agribusiness News September 2024 – Milk

3 September 2024Milk production data

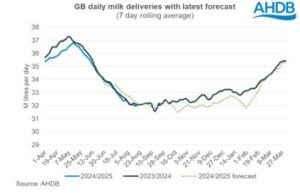

The latest GB monthly milk production data from AHDB is estimated at 1,023m litres for July, which is 252m litres less than the previous month and just 0.4% less than July 2023. Daily deliveries were 31.94m litres for the W/E 17th August, 0.4% below the previous week and 0.4% down on the same week last year. The UK milk volume for July is estimated at 1,247m litres.

Farm-gate prices

Milk prices from the main Scottish milk buyers available at the time of writing are shown below. The trend for processors here and south of the border is still positive with milk price rises on the back of low seasonal production and commodity prices rising on the back of product shortages.

Dairy commodities & market indicators

Wholesale prices for dairy commodities continue to rise, most notably for cream and butter which were both up 7% on the month. Low milk volumes and lower butterfat levels with cows at grass has contributed to little availability. Butter production has declined on the back of limited availability of cream and along with demand picking up after the holiday period, is helping bolster prices. The market for SMP has been quiet, with little change in the August average price and mild cheddar is up just 2% on July, with reports of mixed demand. As a result, the AMPE price rose more than the MCVE price mainly due to the increase in the butter component, with little change in the butter milk powder and skim milk powder component of AMPE pricing.

The Milk Market Value indicator represents the average market value of milk and is derived from how that milk is utilised in the UK. It is currently at 41.29ppl for August (+1.48ppl from July). This is the 4th increase in a row and movements in this indicator are often reflected in farm-gate price changes in three months’ time, meaning that milk price rises look likely to continue into the autumn. Margins over purchased feeds should also improve as prices for protein supplements have dropped over the last month; wheat distillers’ dark grains are back about £20/t to ~£275/t and soya has dropped about £15/t to ~£370/t for full loads delivered to the central belt.

Bluetongue update

The UK’s chief veterinary officer is urging farmers to remain vigilant regarding the purchasing of livestock from bluetongue affected areas in Europe. The number of cases has been increasing rapidly, with over 4000 new cases since May, with Belgium, Germany and the Netherlands being particularly affected. In addition, France, Luxembourg and Denmark have also seen their first ever cases. The risk level for introduction of the disease into GB remans at “medium”.

Dairy herds in decline

Recent data from the Scottish Dairy Cattle Association show that the number of dairy herds in Scotland has fallen by 21 in the first six months of 2024, with 773 herds remaining. Dairy cow numbers now stand at 180,250, 398 fewer since the start of the year, with the average herd size now 233 cows. A similar trend was seen in AHDB’s survey of major milk buyers in April 2024, estimating the number of GB dairy producers to be 7,130, down 440 on the previous year (-5.8%). Despite this, milk production for the 2023/24 milk year was only back 0.2% on the previous year, with milk volumes per farm increasing. As well as the low milk price in relation to cost of production, other reasons thought to be behind farmers leaving the industry include good cull cow prices, sustained inflation pressure on inputs and the cost of borrowing with increasing interest rates. Further significant investment required to comply with NVZ regulations and slurry storage may also have been a decisive factor.

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service