Business and Policy March 2026 – Global Markets Outlook

2 March 2026Global trade update

Global trade news seems to have been dominated for months by tariffs imposed by the Trump administration. Levied upon competitors and allies alike; the traditional patterns of global trade are undergoing a significant shake-up, with the rest of the world’s economies trying to react in agile and wise ways to avoid being victims of collateral damage. The current climate of uncertainty makes it difficult or impossible to take long-term business decisions, especially for agricultural businesses which import from or export to other countries. This article gives an overview of the key forces shaping global trade in 2026 and provides an update on how businesses are reacting.

The Conflict with Iran

Dominating world headlines at the end of February, following months of speculation, the America and Israel military attack on Iran has caused major disruptions to shipping in the Strait of Hormuz, resulting in a sharp rise in oil and gas prices and falling airline share prices. With around a fifth of the world’s seaborne oil and 20% of its liquefied natural gas trade flowing through the waterway between Iran and the UAE, even short-term hold ups will cause a major impact on world energy supplies which will have knock on effects on fertiliser and other agricultural commodity costs as previously witnessed when the Suez canal was blocked in 2021.

Headwinds for Scotch whisky

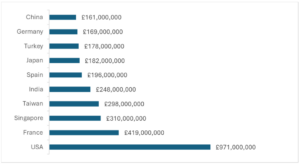

The whisky industry has felt the impact of American tariffs: In the eight months following the 10% tariff imposed on all UK goods in April 2025, exports of whisky to the USA have dropped 10% in volume and 7% in value. This is key, as whisky is a valuable export for Scotland, and the USA is the largest market (Figure 1).

Figure 1: Top ten export markets for Scotch whisky in 2024, by value. Figures rounded to nearest million pounds. Source: Scotch Whisky Association.

This sharp drop in revenue is having effects rippling across the Scotch supply chain:

- Diageo reported that they are currently sitting on £6.1 billion in inventory (including Scotch and other spirits) as a result of supply outstripping anticipated demand.

- Diageo has halted production at the Roseisle maltings (until at least June 2026) and dialled back production at the Teaninich Distillery in Easter Ross; Glenmorangie Distillery has also paused production (scheduled to resume this spring).

- As single malts with age statements take years in the making, due to the current glut, there is a reported shortage of storage space for maturing casks.

- Barley demand has weakened, down from around 1 million tonnes to around 700,000 tonnes expected for the coming year.

- Producers have had trouble securing barley contracts this year due to the contraction in the market and pause or close of maltings.

Slackening demand is bad news for suppliers to the whisky industry, and matters could go from bad to worse: On 4 July 2026, an American tariff on single malts (imposed during a row about subsidies to Boeing and Airbus) will come back into force, unless action is taken to avoid this, increasing the surcharge on these whiskies for Americans to 35%.

Strengthening trade with other partners

To protect UK business growth, Prime Minister Kier Starmer has been seeking to expand markets by lowering trade barriers with other nations: In July 2025, the UK secured a free trade deal with India, with leaders agreeing to roll back their 150% import tariff on Scotch whisky. This has been decreased to 75% and will fall to 40% over the coming decade. The deal is the most significant trade agreement since Brexit (which gave the UK the ability to cut deals of this nature) and is forecasted to deliver a £190m gain to the Scottish economy. India is the largest market for Scotch by volume, with importers buying large quantities of spirit and blending Scotch with whiskies distilled domestically.

In January 2026, a deal was reached with China, cutting whisky import tariffs from 10% to 5%. While not as significant a whisky trading partner as the USA or India, China’s Scotch imports are growing, and the deal is projected to be worth £250m to the UK economy over the coming five years.

For next steps, the chief executive of the Scotch Whisky Association has called on the UK Government to work on securing trade deals with Thailand, the Mercosur bloc of South American nations, and the Gulf States.

Pivoting for resilience

The current situation in the whisky industry exemplifies some of the risks driving the ways global businesses are adapting to the current geopolitical climate. The history of global trade has been a story of increasing globalisation, optimising for efficiency, scale, and profit maximisation. However, when long-established trading partnerships can be thrown into jeopardy overnight, many businesses are making changes in their supply chains to protect against these new threats.

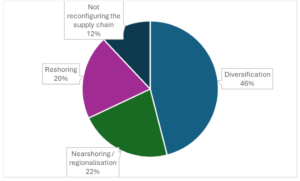

Both open conflicts as well as strategic alliances can have repercussions for businesses: While certain countries may not be subject to tariffs, diplomacy with allies sometimes requires countries to restrict trading with certain nations. Those who rely on China for inputs are considering “dual supply chains,” in which they continue to source from China while hedging through buying from another location, one type of diversification (Figure 2). Within the USA, 40% of businesses have reported that they are planning to increase the proportion of USA-made products within their supply chains (i.e. ‘reshoring’) due to political pressure.

Figure 2: How global businesses report they are geographically reconfiguring their supply chains due to geopolitical climate. Source: Economist Impact Trade in Transition survey.

With the global trade map being redrawn, there is an opportunity for the UK to take advantage of the upside as a neutral, trusted trading partner. The most common strategy to mitigate geopolitical risks reported by global businesses is ‘friendshoring,’ or relocating supply chains to politically aligned countries or neighbours, which 34% of which are implementing.

Overall, the most common response to the turmoil created by the United States has been to diversify trading partners for both imports (by sourcing from multiple locations) and exports (by expanding into new markets).

Closer to Home

For the Scottish agricultural sector, the key takeaway is that global trade has entered a more volatile and politically shaped era, which shows no sign of settling down. The impacts on key sectors such as Scotch whisky show how quickly external shocks can ripple back to farmgate demand, which have knock-on effects for barley purchases, contracts, and prices. At the same time, new agreements with India and China demonstrate that market diversification can create fresh opportunities, particularly in fast-growing economies with expanding middle classes.

Looking ahead, resilience will matter as much as efficiency. Farmers and processors may wish to explore the export destinations of their outputs, maintain flexibility in cropping and supply arrangements, and explore relationships linked to emerging markets rather than relying heavily on any single destination, where possible.

In a world of tariffs, ‘friendshoring’, strategic realignment and businesses that combine high-quality production with diversified routes to market are likely to be best placed to navigate whatever the next shift in global trade brings.

Brady Stevens; brady.stevens@sac.co.uk

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service