Agribusiness News August 2023 – Arable

31 July 2023Cool, damp start to harvest 2023

July saw a tentative start to winter barley harvest for Scotland as inclement weather made harvesting a stop/ start affair. Standing crops still show promise despite the unsettled conditions and there is still the potential for a good wheat and spring barley harvest given a fair August. These weather concerns continue to drive the market in the short term aside from the conflict in Ukraine and despite the recent rally in wheat price as Russia steps away from the export grain deal, the market has an underlying value factored in already in terms of ‘war premiums’ which will continue to underpin values. However, for the UK, fundamentally not a lot has changed. There remains a historically high level of feed grain carried over from last year and with another large crop possibly to come, we will need to see additional demand soon, for what is currently an uncompetitively priced export commodity. The value of the local Scottish distilling market for wheat cannot be underestimated in this context especially as in the coming months wheat will inevitably continue to be exported out of Russia and Ukraine by road/rail and through other ports and at very competitive prices.

Further afield, extreme temperatures in the Mediterranean threaten spring crops of barley and maize although this contrasts with cooler wetter conditions in northern Europe. Scandinavia planted its spring malting barley late and Denmark is expecting yields down by a quarter, good news for UK malting barley growers. Across in the US, the weather outlook is also looking less favourable, especially in the deferred forecasts, with talk of hotter, drier conditions, which again may have a major impact on final spring crop yields and production.

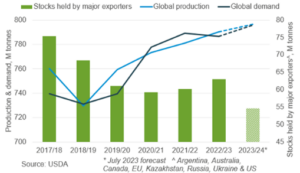

Fig 1

The USDA July report unexpectedly increased its forecasts for the US wheat and maize crops and contrary to industry expectations. With a larger US wheat crop offset by smaller wheat crops expected in the EU-27, Canada, and Argentina; global wheat supply and demand is forecast to be finally balanced, with stocks held by the major exporting nations at its lowest level (54.7Mt – Fig 1) since 2012/13.

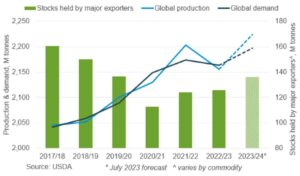

Even with the US maize crop being revised upward, changes at the total grain level globally, are small. Total global grain production is still expected to exceed demand by a large surplus (26.5Mt) (Fig 2). On the upside, the global tightness of wheat supply might mitigate the downward pressure expected in maize markets and the premium over maize futures could therefore strengthen.

Fig 2

Break-crop markets

Feed oat values continue to be supported by the main buyer Spain with large premiums over feed barley. Generally, European oat markets continue to be supported by the lack of harvest sellers.

At the end of July, UK rapeseed prices saw added benefit from the weaker sterling/euro following the release of lower inflation figures. Farm selling increased dramatically through mid-late July as harvest ex-farm levels surpassed £400/t for many, an increase of £100/t in comparison to only two months ago. Whist too early to draw conclusions on UK yield and quality, Eastern Europe appears to be faring better than West (with disappointing yields in France).

New crop bean prices have risen in line with other commodities and domestically demand for feed beans has increased as compounders look to reduce their reliance on imported protein.

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service