Agribusiness News January 2023 – Sheep

22 December 20222022 Highlights

The domestic and global demand for sheep meat has been evident through 2022, combined with a tight global supply, which has sustained prices of all classes of sheep throughout the year. Following the conflict between Russia and Ukraine, the cost of inputs have soared on farms. With feed, fertiliser, fuel showing huge rises on the year, margins have tightened. We have also seen three prime ministers in the year, with changing policies and an increase in the cost of finance, which has been an additional hurdle to the sector.

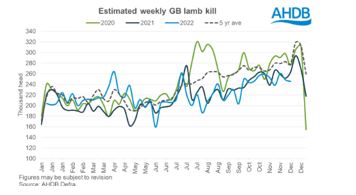

We have seen the contrast between the East and West. With the East having drought conditions in the summer which limited grass supply, while the West reported high levels of rainfall and an ocean of grass. The effect to the sheep on the East has largely shown poor growth rates in lambs and low condition in ewes. This has resulted in a lower than normal numbers being slaughtered in the second half of the year (2022 = blue on below chart).

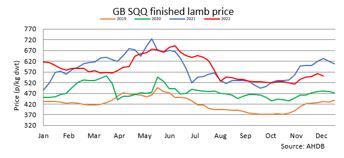

The cull ewe trade has been exceptional, further showing the tight domestic and global supply of sheep meat. The lamb trade opened the year exceptionally at 616.50p/kg SQQ DW, which exceeded the past three years. This tailed off throughout the spring has supply increased before taking another spike in the summer. Unlike a typical year, this summer trade continued, with the seasonal slip being about a month behind normal due to both high demand for lamb, and the supply being tight with the drought. To date (16/12/22), we have not seen the high price we finished with in 2021, but we are still well above the 5-year average.

What does 2023 bring?

Given the high demand and tight supply of sheep meat across the globe, prices should be sustained going into the New Year. Consumption of sheep meat within the EU is set to increase by 0.20% per year until 2032 due partly to more people experimenting with different meats, migrating to the EU/UK from out with the EU and religion.

The much-awaited trade deals with Australia and New Zealand will come into play in the New Year. However, they will concentrate on markets with easier access e.g., Asia, this is especially true for New Zealand. With the lower production costs for the Australian and New Zealand lamb, the price gap will remain large compared to the EU lamb. As of the week ending 03/12/22, this price gap was €3.76/kg (NZ lamb = €4.76/kg DW and French lamb = €8.52/kg DW).

It is forecast that consumers will take more interest in the supply chain and how sustainably produced their food is. This offers a massive opportunity for Scotch lamb as we adapt farming systems to be less reliant on expensive inputs and maximise the assets of the land e.g., grassland production.

Kirsten Williams; 07798617293

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service