Agribusiness News September 2022 – Beef

1 September 2022Beef prices steady up

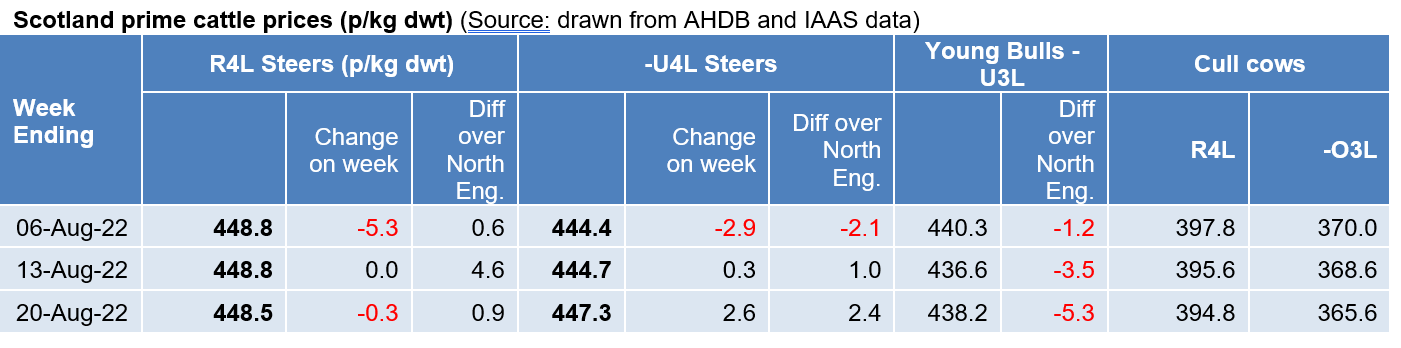

The finished beef price has steadied this month and currently sits around 448p/kg for a R4L steer in Scotland, with the equivalent worth 443p south of the border. Numbers forward appear to be a bit tighter, with demand from the retail sector slow as the consumer has returned to pre covid habits coupled with summer school holidays. This results in a reduced demand for beef as many families holiday abroad or change their weekly buying habits.

As we move further into September and the English schools return then we may see a return to more normal buying habits.

Carcase balance issues

Whilst finished cattle availability has been tighter over the last few weeks; there has been little appetite from the processors to increase the beef price. It is doubtful that increasing the beef price would bring anymore cattle out, and may in fact, have the opposite effect.

Another challenge facing the beef price is the growing demand for cheaper cuts which results in a drop in demand for some steak and other more expensive cuts. With this carcase imbalance quite often the processor or retailer will have to sell those more expensive cuts at a discount price to shift them, resulting in less money overall for that animal. This puts downward pressure on the beef price.

Cow trade still strong

Cull cows continue to be a good trade, currently around 394p/kg deadweight, with good demand from processors and through the live ring. It is worth early scanning Spring Calvers to get them away before any potential dip in trade that may come pre housing when greater numbers of cows are expected onto the market.

With continued high both global and domestic demand for manufacturing beef, it is difficult to see a significant drop in cull cows price as consumers try to reduce their food bills considering the high levels of inflation the country is experiencing.

The concerns regarding the number of cows being culled and the effect that will have on breeding cattle numbers going forward has been discussed often over the last few months.

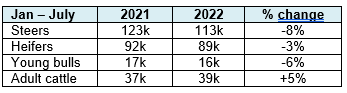

Slaughter numbers

The table below illustrates the changes in cattle numbers slaughtered in Scotland for the first seven months of both 2021 and 2022.

The drop in prime cattle numbers slaughtered was predicted by BCMS data at the start of the year, it was also predicted then that there would be an increase in cull cow slaughterings but not at the levels shown in the above table.

October and November are historically the months where we see the cull cow numbers peak and so it will be interesting to see whether many of these cows have already been slaughtered or if they are still to come forward.

Store cattle

Demand continues to be high for shorter keep stores whilst smaller stores are noticeably cheaper. With the sales of weaned spring born calves starting soon, there is an apprehension that a glut of these younger, lighter animals will come onto the market as breeders try to reduce mouths to feed through the winter. With uncertainty in the long term finished beef price this may cause a drop in value of these weaned calves. However, with harvest well underway in most areas reports are of good straw and barley yields which should help in the decision making process for those with mixed arable and livestock units.

lesley.wylie@sac.co.uk , 01307 464033

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service