MMN March 2024 – Milk Market Update

14 March 2024UK Wholesale Dairy Commodity Market

- Fonterra’s latest on-line GDT auction (5th of March) resulted in a 2.3% decrease in the weighted average price across all products, reaching US $3,630/t. This was the first drop since November, after a run of six positive movements in the price index. While cheddar was up 4% (to $4,277/t), the biggest reductions were seen in skim milk powder (down 5.2% to $2,640/t) and whole milk powder (down 2.8% to $3,286/t). Full results are available at https://www.globaldairytrade.info/en/product-results/

- In the UK wholesale markets, only butter showed a positive movement in price from the last reporting period, up 2% on the back of increased EU demand and tight supply. Butter increased by $600/t in the early February GDT auction and held for the second auction, further stimulating EU prices, with spot trade reaching €6,500/t. Other commodities were back slightly with markets generally quiet, with buyers fairly well covered and waiting to see what happens with prices as milk volumes increase.

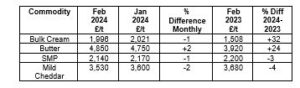

Source: AHDB Dairy – based on trade agreed from w/b 22nd Jan – 12th Feb 2024. Note prices for butter, SMP and mild cheddar are indicative of values achieved over the reporting period for spot trade (excludes contracted prices and forward sales). Bulk cream price is a weighted average price based on agreed spot trade and volumes traded.

- Cream responded slightly to the rise in butter price towards the end of the reporting period but overall there has been little movement in price but it is still 32% above this time last year.

- SMP prices have been stagnant over the last few months with little demand as buyers are well covered. Cheese has also shown little movement, but it is thought that the significant reduction in Irish milk volumes and their sellers pushing for higher prices should bolster the UK cheddar market going forward.

- There was little movement in the market indicators, with AMPE up 0.21ppl from the previous month and MCVE down 0.86ppl. The rise in AMPE was due to the increase in the butter component and the drop in mild cheddar affecting the MCVE price. The Milk Market Value (MMV) for February was 36.95ppl, down 0.64ppl from January, the first decline since September last year. Movements in MMV tend to closely reflect changes in farm-gate prices in three months’ time.

- Defra put the UK average farm-gate milk price at 37.68ppl for January, just 0.24ppl less than the December price. The UK volume for January was 1,238 million litres, which was 1.0% more than the previous month but 0.6% less than the January 2023 volume.

- The March and April forecasted milk prices by The Dairy Group are estimated at 39ppl based on current milk prices and returns from the commodity markets. Due to the poor, wet start to spring, markets will likely be supported as milk supply lags behind last year and could keep any expectations of a decent spring flush in check. As always, farm-gate prices and market returns are highly dependent on spring weather and grazing conditions.

GB Milk Deliveries and Global Production

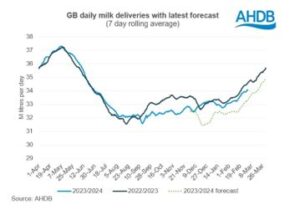

- For the week ending 2nd of March, milk deliveries were up 0.6% on the previous week with a daily average of 34.09 million litres/day. Deliveries are still below the same week last year, down by 1.4% or 480,000 litres less per day. While production is still lower than this time last year, the gap has closed significantly compared to six months ago.

- The estimated GB milk deliveries for January were 1,023 million litres and for February, 973 million litres. Despite the drop in February, milk production is now on its seasonal increase as the spring flush approaches, which normally peaks in early May.

- Global milk production for December from the key milk producing regions was back 0.4% to 804.5 million litres/day, compared to December 2022, equivalent to 3.4 million litres less per day. Apart from Australia and New Zealand, declines were seen in the EU-27, UK, Argentina and the US.

- The biggest decline in the EU was in Ireland, with the December volume down 27% on the previous year. This is due to milk price below the cost of production, very wet weather conditions forcing cows to be housed earlier and new nitrate restrictions coming into force from January 2024.

- Out of the six regions, Argentina showed the biggest drop with production down 7.7% on the back of falling milk prices from the Government’s devaluation of currency and farmers either stopping production, culling cows or feeding less concentrates to lower costs.

Other News

- From April, dairy farmers will see their AHDB levy increase by 33%, from 0.06ppl to 0.08ppl. This is the first rise for 20 years and Chairman Nicholas Saphir said the rise would allow AHDB to increase spending in priority areas identified by farmers e.g. finding new export opportunities and more marketing campaigns.

- New legislation on dairy contracts is now being finalised by Parliament and is expected to be fully implemented by summer 2025. The areas that the new contract reform covers includes:

- Pricing, with greater transparency.

- Cooling off periods.

- Notice periods.

- Contract agreement by both farmer and processor.

- Exclusivity – with farmers able to sell their milk to more than one processor.

- Farmer representation.

For more information see:

https://www.nfuonline.com/updates-and-information/dairy-contract-legislation-essential-information/

- A new way of detecting lameness is currently being trialled at Agri-EPI’s Southwest Dairy Development Centre in Somerset. The AI-powered device, called Hoof Monitor, identifies lame cows through thermal imagining. This detects a rise in leg temperature due to an increase in blood flow, which is a clear indicator that something is wrong in the cow’s foot. The monitor can be mounted somewhere (e.g. a cattle race or on exit from the milking parlour) where the cows walk past to analyse their feet and legs. The device is thought to detect lameness much earlier than current methods and was developed by ex-army man James Wilcox who has expertise in drone technology and runs a small holding in Devon.

Monthly Price Movements for March 2024

- Both First Milk and Müller have announced price rises of 0.75ppl and 1.0ppl respectively for April.

lorna.macpherson@sac.co.uk; 07760 990901

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service