MMN May 2024 – Milk Market Update

9 May 2024UK Wholesale Dairy Commodity Market

- Fonterra’s latest on-line GDT auction (7th May) resulted in a 1.8% increase in the weighted average price across all products, reaching US $3,708/t. This was the third consecutive rise in the GDT price index, although the previous auction only returned a 0.1% rise. Cheddar showed the biggest increase, up 8% to $4,257/t, followed by whole milk powder (+2.4% to $3,350/t). Out of the eight products on offer, only lactose fell in price from the previous auction. Full results are available at https://www.globaldairytrade.info/en/product-results/

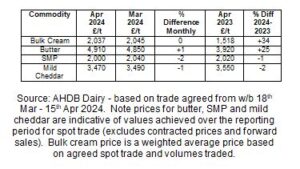

- Similar to the previous month, there was little movement in domestic wholesale commodity prices, with markets subdued and little buying activity. Buyers are pretty well covered in the short-term and have been anticipating prices to drop as the seasonal increase in milk production picks up. On the other hand, sellers are not keen to drop their prices until there is a clearer picture of what future milk supplies will be like.

- Only butter showed a positive price movement, with butter stocks thought to be tight from reduced production on the back of little growth in milk volumes. In addition, the significant decline in Irish milk production is also affecting the market.

- The slight drop in mild cheddar comes off the back of little buying activity and relatively weak demand being reported by some processors. Price is also thought to have come under pressure from imported product from New Zealand.

- Both market indicators fell slightly into April, with AMPE down 0.48ppl from the previous month and MCVE down 0.71ppl. The drop in AMPE was due to the fall in the SMP component and the drop in mild cheddar and whey powder affecting the MCVE price. The Milk Market Value (MMV) for April was 35.68ppl, down 0.67ppl from March and the third consecutive monthly decline.

- Defra put the UK average farm-gate milk price at 37.42ppl for March, 0.57ppl less than the February price and in line with the recent movements in MMV and AMPE. The UK volume for March was 1,322 mlitres, which was 12% more than the previous month but the same as the March 2023 volume.

- According to The Dairy Group, the estimated cost of production for the 2023/24 milk year was around 42ppl. While feed prices fell, they were offset by higher fixed costs. In comparison, the weighted rolling farm-gate milk price averaged just 37.3ppl. Going forward, fixed costs will keep rising (due to inflation at 3-4%), along with higher feed costs as the wet weather will impact on next winter’s feed prices. Their forecast for milk price is little change, with the Defra farm-gate milk price to firm marginally to around 38ppl by July, increasing slightly to nearly 39ppl by September. With no sign of production costs easing, current milk prices are not sustainable in the long-term.

GB Milk Deliveries and Global Production

- For the week ending 27th April, milk deliveries were 0.8% up on the previous week with a daily average of 36.10 mlitres/day. However, deliveries were 2.3% down on the same week last year, equivalent to 850,000 litres less per day. Cold wet conditions throughout April have limited grazing opportunities but the warmer weather at the start of May will see grass growth rates increase significantly and boost milk production, although it is unlikely to come close to the peak of 36.79 mlitres/day seen in May 2023.

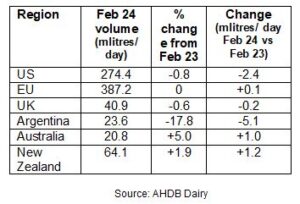

- Global milk deliveries for February showed a mixed picture across the main milk producing regions (see following table). Daily deliveries were 813 mlitres, down 0.7% (5.5 mlitres/day less) compared to February 2023.

- In the EU, Irish milk volumes declined by 13.3% and Germany showed the biggest increase in volume, up 81 mlitres (3.3%) for February compared to the same month in 2023. US milk volumes have dropped on the back of a reduction in size of the national herd from heavy culling. The huge reduction in Argentinian milk has been due to heat stress conditions (both very high temperatures and humidity levels), as well as the financial crisis and triple digit inflation. In March 2024, their inflation rate increased to 287.9% from 277.1% in February 2024.

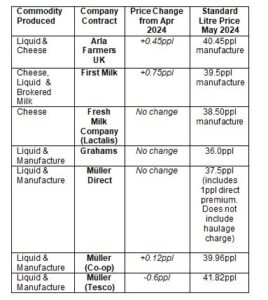

Monthly Price Movements for May 2024

Other News

- Müller has announced a 0.5ppl price rise for June, taking its direct suppliers up to 38ppl (which includes the 1ppl premium for those meeting the requirements of the Advantage scheme).

- As of 1st May, cases of HPIA (highly pathogenic avian influenza) have been detected on 36 holdings across eight states. It is now mandatory that all lactating dairy cows must test negative for HPIA type A before being moved between states. The Food and Drug Administration in the US is adamant that the threat to human health is negligible, as pasteurisation inactivates the H5N1 virus. The spread to the virus in cattle is thought to be either due to the feeding of infected ground up poultry carcases or from infected wild birds gaining access to cattle sheds. Defra are closely monitoring the US outbreak and currently state that the UK dairy cattle population are not thought to be at risk, given that reports of the avian flu virus in birds and poultry are currently very low.

- The new legislation on milk contracts, The Fair Dealing Obligations (Milk) Regulations 2024 will apply from the 9th July 2024 for new milk purchasing contracts. Existing contracts have a further 12-month transition period to ensure compliance and should be completed by 9th July 2025. For more information on the legislation please visit: https://www.nfuonline.com/updates-and-information/dairy-contract-legislation-essential-information/ and https://www.legislation.gov.uk/uksi/2024/537/body/made

- Is the camel the future for sustainable milk production? It is in the Middle East! From a nutritional perspective, camel milk is lower in fat and higher in lactose compared to cows milk and it is also high in vitamin C. With our changing climate, camels are well adapted to cope with hot dry conditions and freezing temperatures in the desert at night. They produce less methane than other ruminants and can survive on little water and roughage for days. While the camels in Africa are reported to produce between 1000 to 2700 litres of milk per lactation, camels in Afghanistan and Pakistan are very high yielding, producing up to 30 litres/day and in some very intensively bred animals, up to 40 litres/day. Intensive camel farming is big business and a rapidly expanding industry. The largest intensive camel farm in the UAE has over 10,000, with fattening units for the male camels for meat production. By the end of the decade, it is predicted that the global value of the market for camel milk will range from US $2 billion to $13 billion.

lorna.macpherson@sac.co.uk; 07760 990901

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service