Spring Barley – Harvest 2026 Prospects

14 July 2026Spring barley crops enter the final month before harvest, facing one of the most significant shifts in market fundamentals seen for several years. After a prolonged period of oversupply, Scottish and UK growers have responded decisively by cutting spring barley area, particularly in Scotland where plantings are estimated to be down by around 16% compared with last season.

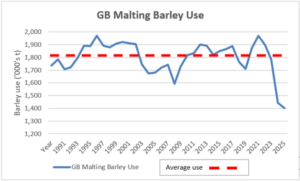

The reduction in area comes against a backdrop of weaker demand from the malting and distilling sectors. UK malting barley use fell sharply during 2025/26, with brewers, maltsters and distillers reducing barley usage by almost 20% year-on-year, while total UK brewing, malting and distilling demand dropped to its lowest level since 2008 (Fig 1). Scottish distillers alone reduced malting barley consumption from around 1.02 million tonnes in 2024 to approximately 826,000 tonnes in 2025 — a fall of almost 200,000 tonnes or 19%. Consumption is forecast to recover only gradually, reaching around 904,000 tonnes by 2028, still below levels seen in 2024.

Against that backdrop, the reduction in spring barley area is beginning to look like a necessary correction rather than a concern. Current estimates suggest the sharp fall in Scottish sowings could remove around 250,000-300,000 tonnes of production from the market, depending on final yields, helping move supply and demand back towards equilibrium.

Figure 1. GB Malting barley use 1990-2025

Crop prospects entering mid-July remain encouraging. Timely rainfall and favourable temperatures across much of Scotland have supported strong yield potential; crop conditions are generally considered good.

The economics of malting premiums have also changed markedly. Prior to the recent downturn, distilling premiums of £40-60/t over feed wheat were relatively common, and during tighter years premiums occasionally exceeded £70/t. By harvest 2025 many contracts were trading at £180-220/t against feed wheat values around £168/t, leaving premiums closer to £15-35/t depending on movement and specification. Current indications for harvest 2026 suggest distilling contracts in Scotland are likely to be in the £170-190/t range compared with feed wheat values of £175-180/t, leaving little more than a £0-15/t premium for many growers and significantly increasing the importance of yield and production costs in rotation decisions.

Global influences continue to matter. The easing in oil price following the initial Iran ceasefire has reduced pressure on grain production costs, although fertiliser values remain stubbornly high. World grain stocks are forecast to tighten slightly in 2026/27, with the global stocks-to-use ratio equivalent to around 88 days of consumption compared with over 95 days only a few years ago. Nevertheless, abundant global maize supplies continue to cap feed grain prices internationally and limit upside potential for barley values.

For growers, the message ahead of harvest is one of cautious optimism. A smaller crop and a more balanced market offer a better opportunity for spring barley prices to stabilise, but quality and marketing discipline will remain critical in securing premiums in what remains an oversupplied marketplace.

Mark Bowsher-Gibbs, SAC Consulting

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service