Agribusiness News February 2025 – Sector Focus: Pigs

31 January 2025Stable prices and sustained profitability are not words usually associated with the pig sector; however, this sums up the fortunes of the pig sector nicely for 2024. This is much welcomed and while investment is now happening again, much of this is aimed at improving efficiency and meeting environmental or welfare standards as opposed to expansion.

Prices continued to drift very slowly downwards throughout 2024, losing around 8 ppkg over the year or around £7 per finished pig. Despite this, reasonable margins continue to be made with the fundamentals remaining the same – a much smaller herd than even a few years ago with the country being little more than 50% self-sufficient in pig meat. There are clouds on the horizon however, EU pigmeat is becoming increasingly more competitive, the threat of exotic diseases entering the UK and the lack of new entrants wanting to farm pigs or work in the pig sector.

Standard Pig Prices (SPP EU Spec): Prices started 2024 just under 214 ppkg then slowly crept downwards through the year, falling to just over 206 ppkg at the end of December (AHDB).

EU prices influence the UK market heavily and a major concern is the widening of the price differential between UK and EU prices. This has widened to historical highs of over 40 ppkg in recent weeks which means EU pig meat is much more competitive, more attractive to UK buyers and is potentially displacing UK product on supermarket shelves. The recent Foot and Mouth outbreak in Germany has seen a ban on imports, providing some support to domestic supplies.

Slaughter Weights: Slaughter weights still remain historically high at just over 91kg (AHDB) although this may in part be due to the effects of the festive season on working days in the processing sector causing a backlog. The contraction of the UK sow herd in 2021 and 2022 and no signs of recovery in numbers has meant a significant reduction in finished pigs coming forward. Although this is mitigated in part by heavier carcass weights and productivity gains in the breeding herd.

Cull Sows & Weaners: Cull sow prices have dipped sharply in recent months, following EU pigmeat prices, dropping to around 60 ppkg (T.V.C.) in early January with further pressure due to the foot and mouth outbreak in Germany. Weaner values have remained consistent and although many weaners are on supply contracts; there are still free-market or surplus weaners which have found more interest from specialist finishers in recent months, particularly in light of falling feed prices and stable prices offering more confidence that sufficient margins can be made.

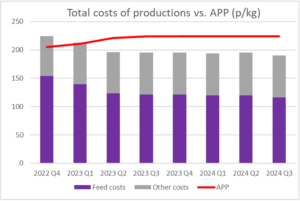

Costs of Production: The latest published margins from AHDB (for Q3 of 2024) showed pig producer margins have risen over the last quarter to 21.90 ppkg (£19.40 per pig), up from 16 ppkg and £15 per pig in Q2.

While pig prices remained fairly constant, costs of production fell by 5 ppkg due to falling feed prices. Feed made up 61% of the total costs, falling to 116 ppkg or £104 per pig. While this represents the seventh consecutive quarter of positive margins, there is still some way to go to make up for the preceding ten quarters of mostly heavy losses. It has been sufficient however, to provide enough confidence for producers to start re-investing in their businesses again. Making businesses more resilient and efficient as well as meeting increasing environmental and welfare standards seems to be the main focus for investment, as opposed to increasing numbers and expanding their businesses.

Figure 1. GB All Pigs Price (APP) vs. Cost of production Oct 2022 to Sep 2024, (Source: AHDB Pork)

Marketing: Three UK pig marketing groups – Scottish Pig Producers (SPP), Scotlean and Thames Valley Cambac have announced they are merging to form The United Pig Cooperative. By joining forces, the groups’ aim is to give independent producers more clout in the marketplace. The United Pig Cooperative will be the largest supplier of support services to independent pig producers in the UK with the official announcement also highlighting enhanced market effectiveness, operational efficiency and member support to provide a more sustainable future.

George Chalmers, george.chalmers@sac.co.uk

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service