Agribusiness News May 2024 – Beef

1 May 2024April sees finished price increase

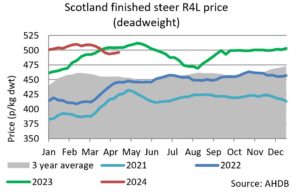

For week ending 20th April, finished beef price in Scotland for R4L steers and heifers is sitting at 496p/kg (+1.3p on week) and 498p/kg respectively. After the previous month saw finished prices drop by 30-35p/kg/dwt, finishers will welcome prices pushing upwards.

The numbers of cattle coming forward for slaughter are not plentiful and continue to trail behind 2023 levels. Going forward it is anticipated that cattle supplies will tighten further by mid-May which should support prime cattle prices. In late spring/early summer 2023 prices were at a high level of 515p/520p/kg and so finishers will be hoping that this is repeated in 2024.

Store markets

Usually during April, auction marts see cattle intended to be put to the grass coming forward but there has not been the same appetite to purchase from finishers due to the challenging weather and ground conditions. With finishers not seeing an increased finished price, but a falling return, store cattle prices have fallen in April. For some prices have fallen in the region of 20p to 30p/kg liveweight. Store cattle are still a good trade, just not at the levels of previous months. Plenty cattle coming forward as farmers struggle for shed space and the difficulty of sourcing straw has also affected store cattle prices. Trade for large forward stores remains strongest as delayed turnout is pushing back the price of grazing types.

As we move into summer, the weather will be a crucial decider in the demand for stores and subsequent pricing.

Dairy-beef trends

Recent figures from AHDB highlight the ever-growing trend for increased dairy-beef bred calves. Registrations of dairy-beef calves have risen by 77% over the past 10 years due to increasing use of beef semen by dairy producers. In 2023, dairy-beef made up 35% of GB prime cattle (12–30 months) slaughter up from 28% in 2019. The majority of slaughtered prime cattle in GB remain suckler-bred. Aberdeen Angus birth registrations to the dairy herd continue to grow. British Blue cross remains the third most popular of all registered dairy-beef crosses however after several years of growth, the number of BRBX registered calves plateaued last year.

Cull cow remains strong

Strong demand for mince and cheaper cuts continues, as consumers look for lower value beef. At time of writing cull cow values are around 406pg/kg/dwt (+4.4p on the week) for R4L grading animals. Trade for cull cows remains buoyant, many beef cows have been at £1,700 to well over £2,000. Like prime cattle, cow slaughter has fallen year on year in Scotland however has risen south of the border. Continuing strong herd decline in England & Wales is set to maintain firm demand from English finishers for Scottish-born beef calves.

With breeding cattle sales kicking off, it will be interesting to see where the demand for breeding heifers is after the realisation now that cull cows are no longer a “by-product” but a “product” which has allowed many to look how they operate a replacement policy with more heifers now coming into herds.

Sarah Balfour, Sarah.balfour@sac.co.uk

Scottish prime cattle prices (Source: drawn from AHDB and IAAS data)

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service