Business and Policy April 2026 – Arable

2 April 2026Market and weather overview

Global grain markets have continued to rise and fall in line with developments in the Iran war and the consequential fluctuations in oil, gas and fertiliser prices. That aside, with global grain and oilseed supplies currently fairly secure, any sign of a lull or dip in Iranian hostilities is tending to see prices come back down. There is, however, a growing question mark over how farmers will react if the recent sharp rises in fuel and fertiliser prices are sustained. If farmer’s margins keep getting squeezed by rising fuel and fertiliser prices and this is not reflected in the market prices for grains and oilseeds, output could start to be impacted as early as the coming harvest.

A useful indicator of US farmer’s intentions is the USDA Prospective Plantings Survey released on 31st March 2026 which could indicate any shifts in crop areas this spring in the United States; for instance – less fertiliser intensive maize or more lower-input soyabeans. Though the timing of the survey means it may not have fully captured the impact of more recent price swings in fuel and fertiliser.

Spring weather in the UK and Europe has been generally dry and favourable giving a good start to spring sowings. The condition of winter crops in the UK is also reported to be good with the AHDB estimating that by 23 March, 82% of UK winter wheat crops were in good or excellent condition. This is the best crop condition score at this point since 2023, with heavy winter waterlogging receding and soil conditions improving.

Elsewhere, the main weather concerns are seen in South America affecting the soya harvest. In the US, drought has been affecting winter wheat in the Southern Plains, although rain is forecast.

In the UK, domestic wheat prices have risen around £5/t in the last month. The Ensus bioethanol plant has recently announced it will re-open “imminently” for an initial 3-month period, potentially requiring up to 100kt of grain per month. Vivergo, the plant’s owners have reopened it following the granting of £100m of UK government support to ensure a domestic supply of carbon dioxide, a vital ingredient for UK food processing and other industries. The doubling of natural gas prices has apparently cut European fertiliser production and related carbon dioxide output. The Ensus plant is particularly vital for Scotland as it offers a large market just over the border when Scotland has a surplus (as it does now) and also draws in English wheat, stopping it heading north. In the last month, UK feed wheat futures are up £5.40/t to £167.65/t for May-26. New crop wheat futures are up £9.50/t to £186.50 for Nov-26 and up £10.70/t to £197.10/t for Jul-26.

Oilseed rape prices in the last month have risen £10/t to around £415/t delivered in Scotland. The main driver has been volatile but mostly high oil prices lending support via the use of vegetable oils in the biodiesel market.

Input costs

The war in Iran has increased the costs of key inputs for crop production; namely fuels and fertilisers. How much have these costs increased? How do these affect growing costs per ha and per tonne? And have grain markets risen enough to cover these costs?

Fertiliser

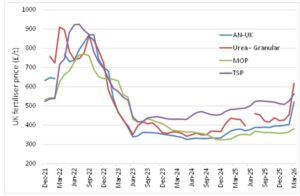

In the last month, the UK ammonium nitrate price has risen by £102/t to £504/t (up 25%) and granular urea has risen £163/t to £618/t (up 36%). The price of potash and phosphate have risen much less, between 5-7% to date. Despite recent rapid gains, the prices of all fertilisers remain well below the highs seen in Autumn 2022, after the Russian invasion of Ukraine when ammonium nitrate reached an eye watering £900/t.

UK Fertiliser prices 2021 – 2026

Source: AHDB

Fuels

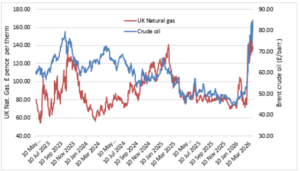

In the last month, UK Brent crude oil prices have risen by 58% to £84/barrel and UK natural gas prices have risen by 76% to £1.36/Therm.

On-farm red-diesel prices have risen around 63ppl to over 135ppl, and kerosene/heating oil has risen a similar amount to around – £1.25/litre although price quotes vary widely.

Oil and gas prices are now higher than after the Russian invasion of Ukraine. Oil prices affect the price of almost everything including transport and the price of plastics; with gas prices having a strong impact on fertiliser prices.

UK Crude Oil and Gas Futures

Source: AHDB

Grain growing costs

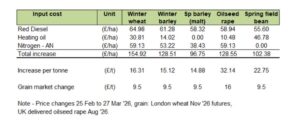

The impact of rising fuel and fertiliser costs will vary by farm depending on how much they have bought ahead. A comparison has been made in the table below on the changes in estimated fuel and nitrogen fertiliser costs for growing and drying cereal, oilseed, and pulse crops in Scotland for 2026 harvest. This assumes that inputs were bought now, though in reality much has already been secured for the current growing season.

Since the war in Iran started on 28th February up to the 27th of March, it is estimated that rising input costs could have added around £15-16/t for cereals, £22/t for beans and £32/t for oilseed rape.

The grain and oilseeds markets have also risen but so far this has only made up around half of the cost increase for both cereals and oilseed rape.

For UK winter crops, the potential erosion of margins in the current crop is not likely to greatly influence the harvest outcome, though farmers may seek to lower fertiliser rates and cut fuel use where they can. For spring crops, however this could be enough to lower plantings particularly of cereals such as spring barley in the UK and maize in the EU/US. There is potential for a rise in fallow area or lower input crops such as beans in the UK and soyabeans in the US.

Whenever we see such big swings in input costs, it pays to recalculate budgets so that true costs and updated sales figures trigger known budgeted prices and margins. It is always better to be horrified than mystified so that opportunities can be taken and risks offset in time where possible.

Anticipated increases in input costs for growing cereal and oilseed crops for 2026 harvest.

Source: AHDB, SAC Consulting

Julian Bell; julian.bell@sac.co.uk

| £ per tonne | May '26 | Nov '26 | Jul '27 | Nov '27 | |

|---|---|---|---|---|---|

| Wheat | Ex farm Scot May | 173 | 178 | 190 | 182 |

| Feed Barley | Ex farm Scot May | 149 | |||

| Beans | Ex farm Scot | 210 | |||

| Milling oats | Ex farm Scot | 120-165 | |||

| Oilseed Rape | Del Montrose | 416 | 405 | 408 |

Indicative grain prices 27th Mar 2026 (Source: SAC/ AHDB)

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service