Business and Policy May 2025 – Cereals & Oilseeds

1 May 2025Scottish Harvest Estimate

The rules of international trade appear to have been swept aside, or at least ignored, since the tariffs from the US were implemented in early April. The World Trade Organization (WTO), of which the US is a member along with 165 other countries covering 98% of world trade, has existed to lower barriers to trade for the economic benefit of all members forming the legal foundation for global trade. The WTO’s ability to counter the impending ‘protectionism’ is currently stifled by the US blocking appointments to the committee involved in resolving trade disputes. Consequently, price volatility of cereals and oilseeds has increased since the announcement of the tariffs, due to uncertainties around global demand, particularly from China who are the world’s biggest buyer. Oilseeds have taken the biggest hit, largely because a bigger share of global production is exported, and China is the top buyer of soyabeans. On average over the past five years, around 44% of soyabean production has been traded globally, compared with 16% for maize and 27% for wheat.

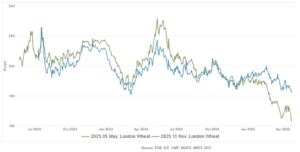

Wheat: Markets continued to weaken across US, European, and UK exchanges amid the macroeconomic instability, strong currency fluctuations, limited fresh demand and favourable global crop weather leading to strong production prospects. The euro’s climb to a 3.5-year high against the US dollar has intensified pressure on euro-denominated grain prices and this strength has reduced the competitiveness of European exports, contributing to wheat contracts falling to fresh lows. May 25 Futures have fallen over the week to currently stand at £167.00/t. The Nov 25 Futures regained lost ground over the week to £184.95/t and traders are increasingly referencing the more stable Nov’25 contract for pricing decisions.

Figure 1: London Wheat Futures 25/04/25

Following a prolonged dry spell in the US wheat belt, US Crop Progress has been helped along by recent favourable weather across the US Midwest allowing corn planting progress to exceed the 5-year average. With no major weather disruptions expected into early May, the usual springtime risk premium in grain prices is fading, keeping pressure on futures

Improving weather conditions have been seen over much of Europe too, especially southern Europe. As a result, the latest European Commission MARS report was ‘cautiously positive’ and France AgriMer announced that 75% of the country’s wheat crop was in good or excellent condition by the middle of April, up from 64% a year earlier.

The news of a bumper wheat crop from Argentina has also added pressure this week as too has increased Russian exports, although volumes are not at the levels of 2024. Without fresh bullish catalysts or weather scares, wheat may drift sideways-to-lower.

Malting barley: One area where the US tariffs could impact the UK industry and growers is in the malting barley markets as the US is the top export destination, by value, for Scotch whisky.

Malting barley markets, for another week, are close to non-existent. From July 2024 -February 2025 usage was down 9% on the same period last season and demand continues to be under pressure due to the cost of living impacting spending within the UK and trends for younger people to drink less alcohol. Crops in themselves are looking well after recent rains, although there is a moisture deficit, and consistent rains are needed to keep the spring barley in good condition.

Feed Barley: Barley price has stayed steadily on the low side. However, although on paper there is a good surplus feed barley supplies are tightening faster than expected with finishers pushing cattle whilst the cattle trade is high. New crop prices should stay under pressure with slow demand, but not until we see farmers starting to make sales. Big-picture market trends will continue to be the main driver of flat prices.

Oilseed Rape: Negative impacts outweigh positives around pricing. The trade remains apprehensive on the potential changes in U.S tariffs on China but are reluctant to react until anything is confirmed. Currency isn’t supportive with the pound undergoing a recovery against the Euro at £1=€1.1723 and the US dollar continues to weaken against a basket of currencies. EU rapeseed production for 2025-26 is forecast up too, at 19.9mt, a rise of 13% from 2024-25 and above the 5yr average, due in part to better weather for oilseeds production. EU rapeseed imports for the current season up as well, totalling 5.18mt to April, up from 4.55mt a year ago, with Australia and Canada increasing their share of EU rapeseed imports compared to last year.

Oats: The UK oat area is expected to increase by 3% for harvest 2025 (Scotland is anticipated to increase its area by 12%). Larger oat supplies outweigh increased consumption, leaving a heavier oat balance this season. Total availability of oats in 2024/25 is forecast at 1.123 Mt. Full season imports are expected to reach just 13 Kt, down 2 Kt on a year earlier. As with other commodities, exports of oats this season have been slow. Full season exports are estimated at 40 Kt. This leaves commercial end-season stocks at 206 Kt, up 82 Kt year on year and 71 Kt greater than the five-year average.

Scottish Farm Business Survey Results

Across the arable sector there were significant falls in net profit for both specialist cereals and general cropping farms of 63% and 53% respectively. This was down from a record high for both sectors in the previous year.

In general cropping farms, agricultural output was decreased by 22%, with input costs down by 8%, and although the overall percentage of support payments was stable at 8% of output year on year, they were down by 13% in real terms in this reporting year.

In the specialist cereal farms, agricultural output dropped by a similar percentage, however support payments only contributed 4% of that drop in total output with the remainder coming from lower grain prices compared to the previous year, and a significantly more challenging harvest in 2023. Input costs were stable, and although fertiliser prices were over one fifth higher than in the previous year, this was offset by decreases in machinery and depreciation costs. The role of support payments in this sector is moderate, at between 11% and 13% of total output.

Mark Bowsher-Gibbs, mark.bowsher-gibbs@sac.co.uk ; 07385 399 513

| £ per tonne | Basis | April '25 | July '25 | Nov '25 |

|---|---|---|---|---|

| Wheat | Ex farm Scot May. July & Nov Futures | 175 | 168 | 184 |

| Feed Barley | Ex farm Scot May, July & Nov Futures | 155 | 165 | 164 |

| Malting Barley | Ex farm Scot | |||

| Oilseed Rape | Del Dundee | 425 | 387 | 395 |

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service