Business and Policy May 2026 – Sheep

4 May 2026Steady into spring

Following strong demand in March driving deadweight prices up to a peak at 867.3p pkg (w/e 28th March 2026), stemming from a tight supply and boosted by both Ramadan and Easter falling close together, we have seen prices ease again slightly going into April. Prices remain well ahead of 2025 figures at >800p pkg deadweight SQQ (AHDB).

The live ring has largely followed a similar trend peaking at the end of March at 408.87p pkg before dropping back to 400.46p pkg although we are seeing a steadying in liveweight price over the last couple of weeks to end the month around 405.53p pkg LW (QMS/AHDB). This is a positive, especially for early lamb producers, as more early born lambs will start to hit the market over the coming weeks with the first couple of new season lambs hitting strong prices in and around 440p pkg.

Cull ewe prices have also remained strong sitting just above 2025 figures at £143.06 for the w/e 18th April 2026 (QMS/AHDB). As strong outlook as we head into the main sales of ewes with lambs at foot in May.

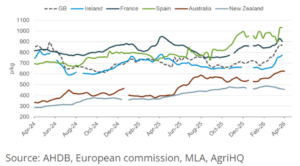

Figure 1 – Global lamb price

GB on the global market

GB lamb prices remain strong in the global market with the price difference with France tightening following a strong March. Spanish prices remain out in front but do continue to show greater market volatility. The Australian and New Zealand prices still very much reflect global markets being two dominant global exporters. The Australian price continues to see a steady rise, again driven by a strong export demand and tightening supplies with prices in New Zealand showing a slight decrease throughout 2026.

Continued contraction of GB sheep flock

AHDB have recently released figures from DEFRA’s December 2025 livestock inventory showing a 2.1% decrease in the national flock with the flock standing at around 20.45 million head – however, data may be subject to change following validation of the Welsh flock.

The largest contraction has been seen from the other sheep and lamb category with the English flock down by 10.4% and the English breeding flock also seeing a contraction of around 2%. This supports previous forecasts of a smaller 2025 lamb crop and demonstrates the impact from a dry spring/summer in 2025. With the reduction in breeding flock, alongside reports of lower scanning’s in some areas, the 2026 lamb crop is expected to contract again slightly with spring conditions also potentially impacting rearing rates in some areas.

With demand for British lamb remaining strong in Europe alongside the contraction of global and domestic supply, this may bode positive for lamb price to keep the market steady as we move through 2026.

Fuel and fertiliser cost and availability are still impacted by global conflicts. Optimising inputs and resources will be vital to maintain margins especially with the silage season approaching. Reducing grassland inputs or a reduced number of silage cuts could impact winter feed resources and next year’s outputs if not balanced carefully.

Australia flock rebuild delayed

Meat and Livestock Australia released their latest industry outlook figures on the last day of March 2026. Following prolonged drought conditions especially in the key production regions in southern Australia, the potential rebuild of the flock may be somewhat delayed, with lamb slaughter forecast to also fall by around 11% in 2026. This may limit further growth in exports in the short term.

Australian lamb carcass weights are expected to continue to increase, however. Driven by genetic gain, lower stocking rates increasing feed availabilty, incentive from processors for heavier slaughter weights, and the rise of intensive feed lots increasing grain-based finishing systems.

Lorna Shaw, lorna.shaw@sac.co.uk, 07796 615719

| Week ending | GB deadweight (p/kg) | Scottish auction (p/kg) | Ewes (£/hd) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 16.5 – 21.5kg | Scottish | ||||||||

| R3L | Change on week | Diff over R2 | Diff over R3H | Med. | Change on week | Diff over stan. | Diff over heavy | All | |

| 28-Mar-26 | 869.3 | 30.1 | 0.0 | -0.1 | 412.50 | -0.9 | 8.6 | 16.2 | 138.16 |

| 04-Apr-26 | 870.5 | 1.2 | 1.7 | 1.3 | 408.20 | -4.3 | 19.5 | 19.9 | 142.75 |

| 11-Apr-26 | 853.7 | 3.2 | 4.1 | 4.2 | 409.60 | 1.4 | 11.4 | 19.8 | 148.88 |

| 18-Apr-26 | 850.4 | -3.3 | 5.6 | 3.7 | 410.00 | 0.4 | 9.7 | 22.7 | 143.06 |

Deadweight prices may be provisional. Auction price reporting week is slightly different to the deadweight week.

Source: AHDB and IAAS Market information

Standard weight 32.1 – 39.0kg; Medium weight 39.1 – 45.5kg; Heavy 45.6 – 52.0kg

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service