MMN March 2024 – Straights Update

14 March 2024UK Cereals Market Update and Global Impacts

Wheat prices in Europe have been capped both by higher global maize supplies expected out of South America, (notably Argentina and Brazil) and slow EU wheat export demand coupled with rising in-house inventories. Maize into the UK is anticipated to increase by 9% this coming season.

UK feed wheat Futures (May 24) currently stand at £159.40 (as of 14th of March) losing the short-term gains previously made in February. The Nov 24 wheat Futures contract appears reluctant to hold above the £185/t mark.

With the UK wheat supply and demand balance 31% tighter this year than last year, wheat exports are expected to be at minimum levels for 2023/24. Exports are currently forecast down from last season by 83% and the UK is expected to be a net importer this season and next, aligning with AHDB’s early indications of a 2024 wheat harvest of between 12-13Mt. Currently fresh farm supplies are just about accounting for the slow consumption offtake and limited buying activity.

For feed barley, export pricing is uncompetitive, and exports are currently forecast for this season down 38% from last season. With a move from winter to spring cropping for harvest 2024 expected, the size of the barley crop remains a key watchpoint for new season export values.

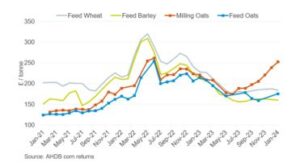

Milling oats prices are achieving highs not seen since June 22, with substantial premiums over feed quality exceeding £70/t in early 2024 (see following graph).

Oat exports this season have hit a stronger pace than expected, especially considering the tighter oat supply and demand balance year-on-year. This season, UK oat exports are in line with the previous five-year average. Looking ahead, oat supply is expected to see a boost for harvest 2024 due to a larger intended planted area. This could see strong exports continue in 2024/25, providing the UK stays price-competitive to the continent.

Global factors mean oilseed rape (OSR) prices have fallen sharply. As of early March 2024, domestic OSR spot delivered prices were over £200/t lower than the peak in 2022. The lower prices combined with the 2023 harvest not delivering, means a drop in the OSR area for 2024 harvest is anticipated. The 20% price drop seen over the last 12 months is partly due to cheaper Ukrainian oilseed rape coming into the European market. Further to that, the overall bearish sentiment of the soyabean market has weighed on prices as record South American soyabean crops are starting to come to the market.

Ex farm prices for cereals and proteins are as follows:

| £ Per tonne | March '24 | May '24 | Nov '24 |

|---|---|---|---|

| Wheat | 160 | 168 | 180 |

| Feed Barley | 140 | 148 | 160 |

| Malt. dist. barley | 240 | 245 | |

| Milling Oats | 240 | 245 | |

| Oilseed Rape | 331 | 333 | 343 |

| Beans | 236 |

Sources – AHDB, United oilseeds

mark.bowsher-gibbs@sac.co.uk; 0131 603 7533

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service