Business and Policy April 2026 – Beef

2 April 2026Finished Prices Continue to Ease

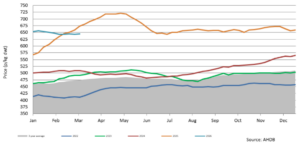

Currently, ‘sticky’ best describes where we are at with finished prices. By the week ending the 21st of March 2026, Scottish prices were sat at 642p/kg deadweight for R4L grade steers, back 1.4 p/kg on the week and 3.4% behind the same week in 2025. GB deadweight prime steer prices also recorded a decline for week ending 21st of March, with average steer prices sitting at 633.6p/kg, down 1.9p from the previous week and 43.2p/kg lower than the same period last year. However, this is still 140p/kg above the five-year average.

With Scottish prime cattle prices remaining relatively flat through March, the 642 p/kg deadweight price for week ending the 21st of March for R4L grading steers is a huge contrast from this time last year, when prices were surging towards £7/kg.

At the time of writing, at the end of March, prices being quoted are around 635-640p/kg/dwt, with reports suggesting that some processors may look to add 2-3p/kg to secure supplies.

Scotland finished steer R4L price (deadweight)

Tight supplies across the UK and Ireland continue to underpin prices. However, despite constrained supply, retail sales continue to disappoint. Demand is simply not there as consumers switch to cheaper cuts e.g. mince and opt to buy chicken and/or pork instead of beef, with consumers looking for best value with regards meat protein. The weather is also currently playing an unhelpful part with regards consumer demand, as it is neither cold enough for roasting joints nor hot enough for BBQs.

Resilient Store Cattle Trade

Store cattle trade continues to be strong, with producers averaging well above £4/kg liveweight. Some producers are receiving around £120 to £150 per head more than this time last year, with top prices of £5-£6/kg being paid for top quality lighter and younger grazing types.

Markets continue to report strong buyer demand, however, in recent weeks there has been a greater demand for lighter, leaner, younger stock to go out to grass, with demand for heavier cattle slipping back. The stagnant finished price will have undoubtedly contributed to fewer heavier stores coming through.

While it is anticipated demand will likely remain strong for the foreseeable future, as finishers look to secure numbers for going to grass; it is still early for turnout, with nights remaining cold and in some parts of the country, the ground is still wet. Although grass is starting to grow, cold weather and wet soil conditions have led to a reduction in grass growth, which is not helping those sitting with reduced silage stocks.

Fodder Shortages

A wet and cold winter on the back of last year’s dry summer has meant that forage supplies are now becoming increasingly tight. Reduced yields and the need to feed additional forage to sheep this year has recently led to strong demand for silage and straw. Tight fodder supplies and rising feed costs are putting further pressure on livestock producers.

Effects of the war in the Middle East

The impact of the Iran war has led to the return of fertiliser price volatility as farmers and crofters are faced with increased costs; with some having seen the cost of fertiliser double overnight.

There are also concerns from suppliers regarding the price and availability of silage wrap which is made from petrochemicals as the war in Iran continues. Fuel prices have also significantly increased, which not just affects farmers and crofters directly but inevitably affects the wider supply chain including livestock hauliers and general haulage costs etc. All this has come at a time when costs for many businesses, both variable and fixed, including finance and borrowings have also continued to rise. Although cattle prices in recent years are as high as they have ever been; margins remain pressured, with the situation in the Middle East, if not resolved quickly, expected to add significant pressure linked to rising fuel and fertiliser costs.

From a beef consumption perspective, as consumers are increasingly met with hikes at the fuel pumps and rising energy costs, this in turn, will impact on their food spending habits. As I have already alluded to, consumers are already looking for the best value in terms of meat protein and opting to buy cheaper manufactured beef; this is unlikely to change in the short term.

Cull Cows – Have prices reached their peak?

Scotland Cull cow (R4L) deadweight price

Cow prices have continued to strengthen, sitting at 565-575p/kg deadweight, up 5p/kg from 2025 levels for the same week, with reports suggesting that there are better deals for well-fleshed R grade cows.

As consumers increasingly switch to cheaper cuts of meat, this is providing additional support for the cull cow market. Several markets have commented that the cull cow trade is as expensive now as it has ever been with strong demand for cows both dead and in the live ring.

Sarah Balfour, sarah.balfour@sac.co.uk

Scotland prime cattle prices (p/kg dwt) (Source: drawn from AHDB and IAAS data)

| Week Ending | R4L Steers (p/kg dwt) | -U4L Steers | Young Bulls -U3L | Cull cows | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Change on week | Diff over North Eng. | Change on week | Diff over North Eng. | Diff over North Eng. | R4L | -O3L | ||||

| 28-Feb-26 | 644 | -0.6 | -8.7 | 640.7 | -2.1 | -6.6 | 634.3 | 3 | 563.4 | 532.4 |

| 7-Mar-26 | 645.1 | 1.1 | -2.3 | 638 | -2.7 | -6 | 630.9 | -6.1 | 560.3 | 534.7 |

| 14-Mar-26 | 640.4 | -4.7 | -5.5 | 639.3 | 1.3 | -6.7 | 634.5 | 10.7 | 559.7 | 538 |

| 21-Mar-26 | 642 | 1.6 | -2.8 | 638.7 | -0.6 | -9.4 | 629.7 | -0.8 | 567 | 544.7 |

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service