Agribusiness News January 2025 – Beef

1 January 20252024 market recap

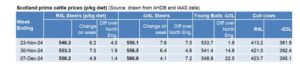

Beef prices started the year strongly, above £5/kg, 8-9% above 2023 levels and 26-27% above the five-year average. Data from QMS showed that to find a time when prices were lower than a year earlier, you had to look back to May 2020. Finished beef prices began 2024 approx. 45% higher than they did in 2020. On the back of strong retail demand in the first few months of the year prices continued to trend upwards as demand continued to outstrip supply.

During January to mid-March, those selling store cattle received record prices, which brought some much-needed positivity to suckler herds who had been feeling the economic pressures. Many averaged over 340p/kg when selling strong continental types, with some markets reporting 400kg well-bred strong Charolais cross bullocks averaging up to 370p/kg. Store cattle and weaned calf prices have continued to be elevated above 2023, with strong demand from England for Scottish suckler bred cattle contributing. It is reported that more than 20% of Scottish stores are now moving into England.

In April, deadweight cattle prices fell which in turn affected the store trade. Reasons included lower consumer demand, good supplies of young bulls coming forward and carcase weights showed a year-on-year increase. Poor spring weather hindered turnout. With sheds at full capacity and feed costs increasing, finishers were reluctant to purchase stores with most unable to get cattle out to grass.

Tightening prime cattle availability has led to prices surging upwards since July, when prices broke back above £5/kg/dwt. Prices were above 15% higher than the five-year average. Simply there are not the cattle numbers out there and finishers and processors are battling to secure numbers, with prices increasing to 555p/kg/dwt in the final few days of Christmas kill to secure orders.

Cull cow prices started the year around 370p/kg/dwt, after a sluggish start to the New Year prices have remained strong throughout 2024, with prices returning to more normal levels relative to prime cattle prices. Cows traded at a premium in Scotland over England and Wales for much of July and August. Prices are currently sitting at 420p/kg/dwt

Scottish suckler herd

The decline in the Scottish suckler herd remains a concern for the industry. ScotEID data reported in September 8,400 (2%) beef cows lost in the past 12 months. Summer 2024 saw an increase in herd dispersals throughout Scotland, however data suggests that approx. 80% were sold into other herds. Lack of succession and lack of labour are some of the reasons behind herds being dispersed alongside the investment required by some to adhere to new government regulations e.g. with slurry storage.

2025 beef outlook

Cattle availability looks to remain tight as we go into 2025, as reduced beef cow numbers further impact supplies. Recent figures from AHDB forecast beef production to fall 6% in 2025 due to increased cow and heifer slaughterings. There are concerns that changes to the Scottish Suckler Beef Support Scheme (SSBSS) will further reduce the national herd size. While prime cattle and store cattle values are at record levels input costs remain high and farmers continue to feel the pressure of trying to improve business and herd efficiency along with the challenges of farming in a nature friendly way.

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service