Business and Policy July 2025 – Beef

2 July 2025Beef prices

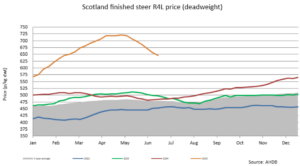

What a difference a month can make! Deadweight steers in Scotland averaged £7.15 per kg in mid-May, up by £2.20/kg compared with the same week last year. However, over the past six weeks finished beef prices have fallen, currently sitting at around £6.40 – £6.50/kg/dwt for R4L grades. At £6.40/kg a 380kg carcase will return a gross price of £2,432 per head.

Market confidence is wavering

It is no surprise that the falling beef price coupled with the availability of young bulls has done nothing to install confidence in finishers, as finished prices closely get to the values paid for some of the strongest stores bought only a few months ago.

While it is normal for prices to drop at this time of year due to the increase in young bulls being slaughtered and less consumer demand for prime cuts in summer – partly due to people holidaying abroad – the current price volatility is not normal.

Cattle prices have fluctuated by £250–£300 per head in two months, however, it is anticipated that prices will lift from mid-July into August as the number of finished bulls coming forward falls.

After several months of incredibly high prices, what is needed now is price stability to allow finishers to make better and more informed business decisions, which inevitability will filter down to suckler producers and install confidence for them to continue to keep cows, despite the various challenges currently facing the industry.

Store cattle

Trade for store cattle has, as expected due to the fall in deadweight prices, fallen back. Demand for strong, short keep stores is still there but buyers are being more selective and are not buying the same numbers of cattle. Limited grass availability in some areas hasn’t helped demand for stores either.

With some bigger store sales scheduled for July, and finishers soon deciding whether to buy store cattle for Christmas, suckler producers will be hoping that the finished price jumps back up or finishers could look to pay less for stores and/or not restock at the same level.

Are prices reflecting consumer demand?

AHDB supermarket figures released at the beginning of June show that over the past 4 weeks, mince and steak prices rose by 6-6.5%, while beef producers have seen their prices fall by 10%. AHDB figures also show consumer demand to be down 2.4%.

Although lamb is traditionally associated with Easter, AHDB released figures from Kantar showing that beef actually performed best of red meats this year with an increase of 9.7% on Easter 2024 prices.

Support for small suckler herds

The recent announcement that the country’s smallest herds will be exempt from the new calving interval requirement of 410 days or less under the Scottish Suckler Beef Support Scheme (SSBSS) in 2026 is a welcomed decision.

Looking Down Under – Australia drops their 2030 carbon neutral target

While our government continues with the need to hit environmental targets, the Australian red meat industry has recently done a U turn on its Carbon Neutral 2030 target, originally set in 2017 – recognising this climate change goal is now unachievable.

Sarah Balfour, sarah.balfour@sac.co.uk

Scotland prime cattle prices (p/kg dwt) (Source: drawn from AHDB and IAAS data)

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service