Business and Policy July 2026 – Arable

2 July 2026Market overview

After several weeks of subdued trading, grain markets have finally found something to get excited about. The intense heatwave stretching across much of Western and Central Europe has forced traders to reassess crop potential, particularly for maize and later-developing spring crops. Prices have responded accordingly, with European futures recovering sharply from recent lows. The interesting part is that Europe and the United States are currently telling completely different stories. European markets are pricing in worsening crop stress, shrinking maize acreage and increasing production risk, while Chicago continues to trade as though very little has changed. Across much of the US Corn Belt, crops remain in good condition, rainfall has generally been timely and weather forecasts continue to favour development.

One of those markets will eventually have to give. For now, European traders are focused firmly on the weather. A second spell of very hot temperatures is forecast during early July, and with many spring crops approaching their most sensitive growth stages, every day without meaningful rainfall increases the risk of lower yields and poorer quality. July has become the month that could define this marketing year.

Wheat

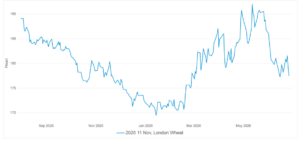

Wheat has inevitably been pulled higher by the strength in maize, although its own fundamentals (Fig 1) remain rather more uncertain (Nov ’26 Futures currently at £177.50/t). The first combines are now rolling through France and early reports suggest yields are around 10-15% below the five-year average. That’s disappointing rather than disastrous, and with much of the French crop now close to maturity, the recent heat is unlikely to cause significant further damage there. Elsewhere, however, the story is rather different. Crops across the UK, Germany and Poland are still filling grain just as temperatures climb towards 40°C in some areas. Whether these conditions leave a lasting mark on yields will become clearer over the next fortnight, but they are certainly enough to keep a weather premium in the market.

Fig 1.UK Feed Wheat Nov’26 Futures

Source: EBC, ICE, CME, Euronext, MGEX, DCE, Barchart Solutions

Not everywhere is struggling. Romania is expected to produce one of its largest wheat crops on record, helping offset losses elsewhere, while Russian and Ukrainian exporters continue to dominate world trade with competitively priced wheat. That remains one of the biggest brakes on any sustained rally. Despite lower production estimates for Russia, global buyers still have plenty of choice, and export competition remains fierce.

Barley

Barley markets continue to divide into two distinct stories. Winter barley is now very much a harvest market. Most old crop stocks have already been sold, consumers appear comfortably covered and attention is turning towards how quickly new crop reaches the market. Assuming harvest progresses without interruption, seasonal selling pressure is likely to build through July.

Malting barley is proving rather more interesting. The prolonged heat across Europe is causing increasing concern over grain quality, particularly nitrogen levels, while early French yields are reportedly well below last year’s performance. Farmer selling also remains notably absent, limiting liquidity and providing a degree of support to prices despite relatively sluggish demand from maltsters.

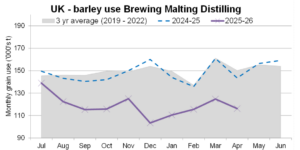

For the UK, the outlook remains finely balanced. Reduced planted area and questions over quality could tighten supplies considerably, although demand as shown in Fig 1, will ultimately determine whether any rally can be sustained.

Fig 2. UK Barley usage (‘000’s t)

Source: AHDB

Oilseeds

Rapeseed has quietly recovered after a period of consolidation. Despite weaker crude oil prices, support has come from firmer palm oil values, uncertainty surrounding sunflower production and continuing concerns over global vegetable oil supplies. The wider oilseed market remains heavily influenced by macroeconomic factors. Favourable US soybean conditions and a lack of fresh Chinese buying continue to weigh on sentiment, while speculative fund activity and currency movements have added to day-to-day volatility. Weather, however, remains the biggest unknown, particularly with the prospect of El Niño strengthening later in the year.

Oats and pulses

These markets remain firmly in “wait and see” mode. Oat buyers are reluctant to commit until they have a clearer picture of both yield and quality, while growers remain equally reluctant sellers at current price levels. The heat across Europe is undoubtedly causing concern, particularly for spring oats, but the extent of any damage won’t become clear until harvest gathers pace. Scandinavian production will remain one of the key indicators to watch, given its importance to European milling oat supplies.

Pulse crops are facing similar challenges. Peas and beans have both come under increasing stress following months of limited rainfall, and although UK vining pea harvest has started with mixed results, it is still far too early to judge the overall crop. Consumer demand also remains relatively quiet, with buyers preferring to wait until harvest quality is better understood before extending forward cover.

Mark Bowsher-Gibbs, mark.bowsher-gibbs@sac.co.uk

Indicative grain prices on 29th June, 2026 (Source: SAC//United oilseeds/AHDB)

| £ per tonne | July‘26 | Nov ‘26 | May ‘27 | Nov ‘27 | |||

|---|---|---|---|---|---|---|---|

| Wheat | Ex farm July. Nov’26/May’27/Nov‘27 Futures | 180 | 177 | 188 | 189 | ||

| Feed Barley | Ex Scot July | 156 | - | ||||

| Beans | Ex farm July | 215 | - | ||||

| Feed Oats | Ex farm July | 123 | |||||

| Oilseed Rape | Del Montrose | 428 | |||||

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service