Business and Policy July 2026 – Beef

2 July 2026Finished prices ‘stand on’

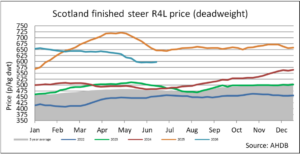

After several months of sharp falls in finished cattle prices, with many finishers having suffered losses of approximately £240/head since February 2026, it looks as though beef prices are now beginning to stabilise around £6/kg deadweight. While the current beef price is undoubtedly seeing finisher margins squeezed, it will come as a welcome relief to finishers that beef prices are looking to swing back in the favour of the producer. For the week ending 20 June, Scottish R4L price quoted was 597p/kg/dwt (+1.8p from the previous week). At the time of writing, reports suggest that Angus sired cattle are now back over 600p/kg. Prices in the live ring are also showing signs of recovery, with auctioneers commenting that price cattle prices have been getting more dear as trade starts to pick up again.

The unsustainable lift in prices in 2025 created disruption in the marketplace and undoubtedly a false economy. While finished prices continue to track behind 2025 levels, compared to 2024 values, prices are up by more than £1/kg/dwt (w/e 22 June 2024 – 484p/kg/dwt). Of note is further falls in Ireland (back 6-7p/kg to an average of £5.41/kg for week ending June 20).

There are no serious price rises anticipated given that demand generally drops throughout the summer. However, with school holidays and consumers holidaying abroad, signs are emerging that the market is beginning to stabilise. This will be a welcome relief for finishers and help to install confidence again.

Consumer demand

Consumer demand for beef remains sluggish, with many households faced with increased food bills. The Guardian News (May 2026) reported food prices such as beef were up 64% in five years, with pasta, frozen vegetables, chocolate and eggs all at least 50% more expensive than five years ago. Demand for beef is limited not just in households but in the catering and hospitality sector also, with butchers also feeling the effect in the marketplace.

With Scotland now out of the FIFA World Cup, hopes for increased beef demand are fading. Although it was hoped that Scotland getting to the World Cup would boost BBQ demand, the recent heatwave has created strong demand for manufacturing beef as the improved summer weather will see consumers get the BBQ going.

Cull cow trade

Similarly to finished prices, cow prices remain fairly static over the past month. For the week ending 20 June prices quoted for cows in Scotland was around 525p/kg/dwt, with reports of 530-540p/kg depending on the abattoir. GB cow prices for June have averaged 530p/kg. In 2025, prices for June averaged between £5.52-£5.58/kg. Notably, data from AHDB for the last four weeks highlights a drop in cow supplies by 2,900 head compared with the same four weeks in 2025. Demand is increasing for cows and manufacturing beef as processors look to meet increased business for BBQ meat, especially burgers.

Store cattle trade remains resilient

Despite fluctuations in finished prices, trade for store cattle remains buoyant with stores continuing to achieve strong prices largely due to simple supply and demand. The contraction to suckler cow numbers means that finishers are having to compete to secure stock, which is helping to maintain store cattle trade. Although store prices are good, finished cattle prices have impacted the trade for heavier stores, with several markets commenting that lighter, longer-keep cattle are topping the trade.

Global supplies and imports

Imported beef is seen in many stores, with notable increase in Australian, New Zealand and Brazilian beef appearing on shelves. Tesco stores have significant levels of ABP Irish beef even though the agreement is 70% British and 30% Irish in a year.

Reports suggest that global beef production is expected to fall by 2.2% in 2026 and highlighted that beef production was already down by 2.5% during the first quarter of 2026. Major contractions are expected in the US, Brazil and China which will likely continue to drive this overall reduction.

Sarah Balfour, sarah.balfour@sac.co.uk

Scotland prime cattle prices (p/kg dwt) (Source: drawn from AHDB and IAAS data)

| Week Ending | R4L Steers (p/kg dwt) | -U4L Steers | Young Bulls -U3L | Cull cows | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Change on week | Diff over North Eng. | Change on week | Diff over North Eng. | Diff over North Eng. | R4L | -O3L | ||||

| 30-May-26 | 596.2 | -3.5 | -11.1 | 583.7 | -6.7 | -22.0 | 580.3 | -1.3 | 522.0 | 500.0 |

| 6-Jun-26 | 596.4 | 0.2 | -9.8 | 586.5 | 2.8 | -20.7 | 586.6 | 2.0 | 524.5 | 500.6 |

| 13-Jun-26 | 596.0 | -0.4 | -13.6 | 589.6 | 3.1 | -23.0 | 581.4 | -9.1 | 530.9 | 494.9 |

| 20-Jun-26 | 597.8 | 1.8 | -11.1 | 592.1 | 2.5 | -19.3 | 593.3 | 4.8 | 525.4 | 495.8 |

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service