Business and Policy March 2026 – Arable

2 March 2026Market overview

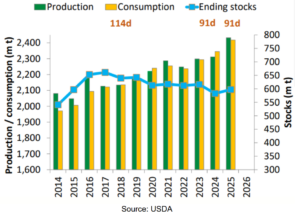

Global grain market pricing remains influenced by heavy underlying fundamentals as over the last 12 months global production has increased by 120Mt, comfortably exceeding an increased consumption demand of 73Mt and leaving a 12Mt increase in holding stocks since June last year. These comfortable global supplies, particularly from large recent harvests, continue to weigh on old crop prices. However, tensions involving Iran and the United States are injecting risk premium into commodity markets. The US and Israel’s attack on Iran have sparked sharp short covering, initially in the energy markets with the potential to quickly spilling over into grains and oilseeds. Firmer crude oil pricing has already lent more visible support to oilseeds.

World grain 2025-2026 supply and demand

Source: USDA

Weather Impacts

Weather is becoming an increasingly important driver as focus shifts to new crop prospects. In the plains plains of the United States, dryness and potential winter kill are under scrutiny as wheat emerges from winter.

In Europe, excessive rainfall has marginally reduced French wheat condition ratings, though they remain well above last year. Meanwhile, South American conditions are seen as pivotal: in Brazil, persistent rains have slowed the soya bean harvest and second-crop maize planting. Delays to maize sowing raise production risks as the dry season approaches.

In Argentina, crop ratings have slipped due to dryness and heat stress and while production is still expected above last year, declining yield potential, especially for soya beans, could tighten global soya bean meal and oil supply.

Black Sea exports remain constrained despite ample supply. War-related logistical disruptions in Ukraine and slower shipments from Russia have reduced export flows year-on-year. Ukrainian maize exports are down roughly 30% and wheat by about 25%. Although this does not signal a global shortage, it redistributes demand toward the EU and the US, tightening the effective export balance outside the region and lending price support.

Crop focus

Wheat

Domestic wheat prices remain subdued and Scottish distilling use is currently down 8% over the last 6 months. The UK is set to see its lowest level of human and industrial cereal consumption in two decades with usage predicted at 9.17 million tonnes, a drop of 1.315 million tonnes compared with 2024/25. Analysts attribute the sharp decline in demand to three main factors:

- the collapse of bioethanol production,

- subdued activity in the brewing, malting, and distilling sector,

- weaker consumer demand amid cost-of-living pressures.

The bioethanol sector has been hit hardest. Vivergo, one of the UK’s main plants, closed last August and Ensus, the other major facility, has remained offline since its scheduled maintenance in September 2025 and is assumed to stay closed for the rest of the season unless Government support intervenes. May-26 UK feed wheat futures are currently trading at £168.65/t

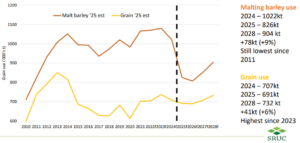

Malting Barley

The malting barley market also remains subdued. Demand from the brewing, malting and distilling sector has softened, with malting barley usage in Scotch Whisky distilling falling from 1.02Mt in 2024 to 826,000 tonnes in 2025, and it is not expected to recover in 2026.

Nationally, AHDB now forecasts human and industrial barley usage at 1.58 Mt, down 214,000 tonnes from last season and the lowest level recorded since digital records began in 1990/91. Analysts cite reduced consumer spending, changing drinking habits, and rising costs as key pressures, alongside reports of distilleries being mothballed and limited export opportunities.

Premiums over feed barley show little sign of widening as buyers remain cautious and largely purchase back-to-back against confirmed sales. Weak sentiment and slow trading activity continue to weigh on prices, and without a revival in brewing demand or export interest, upside appears limited in the short term.

Oilseed Rape

Oilseed markets are more responsive to geopolitical tensions, supported by firmer crude oil values. South American weather remains critical: slower Brazilian soya bean harvest and declining Argentine crop ratings could tighten global soya complex supplies, particularly soya bean meal and oil.

Paris rapeseed futures have strengthened, aided in the UK by weaker sterling. However, prices are technically elevated, increasing the risk of short-term correction. Any Middle East escalation would likely provide immediate additional support.

Oats

Oat markets are quiet but sensitive. Turkish buying has paused after strong recent activity, though favourable tariff conditions could see demand returning.

Feed oat demand has improved, particularly from Spain and Western Europe, while Baltic supplies have tightened amid rising freight costs. UK growers remain reluctant sellers at current prices. With expectations of a reduced planted area for new crop, the market is increasingly vulnerable to adverse weather, which could trigger price strength later in the season.

Mark Bowsher-Gibbs, mark.bowsher-gibbs@sac.co.uk

| £ per tonne | Mar‘26 | May ’26 | Nov ‘26 | |

|---|---|---|---|---|

| Wheat | Ex farm Scot Mar. May/Nov 26 Futures | 161 | 168 | 175 |

| Feed Barley | Ex farm Scot Mar. | 146 | - | |

| Beans | Ex farm | 204 | - | - |

| Milling Oats | Ex farm | 120-160 | ||

| Oilseed Rape | Del Montrose | 406 | 406 | 399 |

Indicative grain prices 25th Feb 2026 (Source: SAC//United oilseeds/AHDB/Hectare)

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service