Agribusiness News April 2025 – Beef

31 March 2025Up and Up

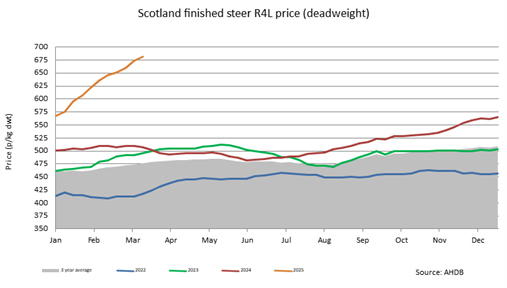

Beef price increases continue with finished cattle prices on the brink of £7/kg/deadweight or close to £3,000 liveweight, with prices expected to surge past £7/kg/dwt at the start of April. Reports are suggesting finished prices could reach £8/kg by the end of this spring. With weekly price increases, beef prices throughout March have continued to set records,. Since the start of the year finished cattle prices have increased significantly, +15p/kg/dwt some weeks.

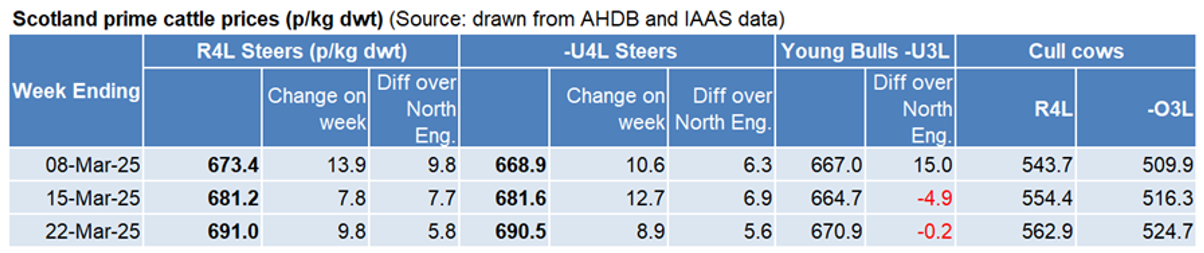

At the start of the March, Scottish finished prices were sitting at 659.5p/kg/dwt and then soared to 691p/kg/dwt, for week ending March 22 for R4L grading steers. Angus sired cattle have reportedly already hit £7/kg. The current demand for beef is also supporting liveweight prices, with averages up on the year with an increased number of buyers ringside. The Institute of Auctioneers and Appraisers in Scotland (IAAS) recently reported an increase of 25% in prices, with many cattle selling for £400 a head more than the same month in 2024.

Despite record prices week after week, there is uncertainty and concerns within the beef sector. The concern is that these prices are unstainable and have yet to be tried and tested on consumers. Are consumers about to see price hikes in April?

The tightening availability of prime cattle in Scotland continues to be the main price driver, with processors battling to secure supplies. Simply, the number of cattle in the UK is falling – slaughterings in February were down 5% compared to 2024 levels. Irish cattle slaughter numbers are also expected to fall by 5% this year. With 77% of UK beef imports coming from Ireland, this will no doubt have an impact going forward. This, coupled with strong demand for beef is fuelling record prices. Rising human populations in the UK and at a global level are set to support demand for red meat in the coming years.

And Up

Strong finished beef prices continue to support store cattle prices, as store cattle trade continues to surpass expectations. Any margin from the current finished beef price is being ploughed back into the store ring. The store producer and the finisher rely on one another to receive a shared level of profitability.

Costs to produce store cattle are high for the majority of beef farmers and the increased returns are welcome. When finishers receive higher returns in the marketplace, they simply return the extra received down the line to the producer. Several finishers have commented that the current of continental sired stores is ‘pricing them out the market’ as they look to native bred cattle to secure numbers.

Continuing the strong decline in herd numbers in England & Wales is set to maintain firm demand this spring from English finishers for Scottish-born beef calves and has the potential to drive store cattle trade further. Several markets have reported higher numbers of stores at sales recently, which suggests that high prices have encouraged some producers to sell calves earlier or sell extra calves instead of taking through to finish. Store prices are predicted to remain firm in April.

Despite record beef prices, our national suckler herd is expected to continue to contract in 2025, with cost of production, market volatility and government policy all contributing to herd dispersals. Farmers looking to retire are maximising their assets by selling cows at a time when prices have never been so high. Herd contraction is further accelerated by the volume of heifers slaughtered, as would-be replacement heifers enter the beef supply chain.

Sarah Balfour, sarah.balfour@sac.co.uk

Related articles

Beef

Rural Business

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service