Business and Policy April 2026 – Milk

1 April 2026Milk production data

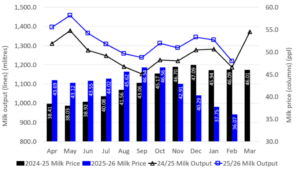

Although milk production continues to be greater than this time last year, with daily production currently at 36.67 million litres for the week ending 21st of March, 0.6% more than the previous week; the percentage increase has slowed through March from +3.2% for the week ending the 7th of March down to +2.2% for the week ending the 21st of March 2026.

For the UK, February production was 1,218 million litres, 31 million litres higher than February 2025. The latest data from AHDB estimates GB volume for February at 986 million litres.

UK Milk Output and Average Farmgate Milk Prices

2024/25 to 2025/26

Farm-gate prices

The Defra farm-gate milk price for February was 36.07ppl, down 1.4ppl from the January 2026 price (3.8%) and 21% less than 12 months ago. Processor milk prices appear to be holding steady with Arla, Müller, and Grahams announcing price holds. While First Milk have announced a 0.5ppl price increase for April, Lactalis are paying 0.5ppl more for their April milk with the price differential is being classed as a hardship bonus to help cover for increased costs. Organic milk prices are currently around 57ppl depending on the contract.

| Milk Prices for Oct/Nov 2025 Scotland | Standard Ltr ppl | ||

|---|---|---|---|

| First Milk2 | April | 30.75 | |

| Müller - Müller Direct - Scotland 1, 3 | April | 34.5 | |

| Grahams1 | April | 34.5 | |

| Arla Farmers2 | April | 34.07 | |

| Lactalis / Fresh Milk Co.2 | April | 31.57 | |

| 1 | Liquid standard litre – annual av. milk price based on supplying 1m litres at 4.0% butterfat, 3.3% protein, bactoscan = 30, SCC = 200 unless stated otherwise. | ||

| 2 | Manufacturing standard litre - annual av. milk price based on supplying 1m litres at 4.2% butterfat, 3.4% protein, bactoscan = 30, SCC = 200 unless stated otherwise. | ||

| 3 | Includes 1.00ppl Müller Direct Premium. Haulage deducted depending on band for 2023 vs 2021 litres, ranging from -0.25 to -0.85ppl. | ||

Dairy commodities & market indicators

The dairy market continues to recover despite ongoing disruption from global conflict. Average prices have risen across all commodities during this period. However, trends have varied: Skimmed Milk Powder (SMP) is the standout performer with prices rising by £300/t over the course of the month to an average of £2,340 (15% increase), conflict in the Middle East has driven prices higher as the 4th largest exporter (Iran) has been removed from the equation. Manufacturers are increasingly looking to use SMP over other more expensive protein options, but dryer space will be a key limitation as we look towards the Spring flush.

The Cheddar market is showing mixed signals, with the average price rising 5% to £3,080/t, stocks are reportedly tight after much curd was sold to drive cashflow. Mature and mild cheddar is said to be difficult to source at this point in time.

The bulk cream market appears to be on a roller coaster, prices have experienced a modest recovery, rising to a peak of £1.77/kg. However, sharply rising freight prices have led to many pulling back from the market and prices have dropped to £1.50/kg. There is a huge volume of cream available globally, which is increasing the pressure on the market and the price is averaging around £1,556/tonne, which is still a 12% rise on the previous period.

The average price of butter was £3,980/tonne which is an 8% increase on the previous period. The butter market has been incredibly volatile, with prices soaring to highs of £4,150 in the middle of the month. European demand increased as New Zealand product was diverted away from the Middle East who then looked to European suppliers. European product continues to trade at a discount to Oceania, but flows in that direction have slowed as rising freight and logistical costs, along with ongoing challenges, prompting traders to step back from the market.

Given the recovery in the price of cheddar and butter, the Milk for Cheese Value Equivalent (MCVE) value has risen by 2.18ppl and the Actual Milk Price Equivalent (AMPE) value has seen a modest rise of 4.6ppl off the back of increased demand for skimmed milk powder. The latest Global Dairy Trade (GDT) auction (17th March 2026) resulted in the price index moving upwards by just 0.1% to a weighted average price across all products of $4,330/t.

| UK dairy commodity prices (£/tonne) | March 2026 | Feb 2026 | March 2025 |

|---|---|---|---|

| Butter | 3,980 | 3,670 | 6,070 |

| Skim Milk Powder (SMP) | 2,340 | 2,040 | 2,010 |

| Bulk Cream | 1,556 | 1,250 | 2,624 |

| Mild Cheddar | 3,080 | 2,920 | 4,020 |

| UK milk price equivalents (ppl) | March 2026 | Feb 2026 | March 2025 |

|---|---|---|---|

| AMPE | 37.35 | 32.75 | 45.09 |

| MCVE | 34.89 | 32.71 | 45.67 |

© AHDB [2026]. All rights reserved.

A survey for the milk sector

Over recent months, the milk sector has experienced significant pressure from global milk supplies and commodity markets, which has led to a sharp decline in milk prices. While the Fair Dealing Obligations (Milk) Regulations 2024 (FDOM24) do not set milk prices, the regulations do require milk purchasers to apply price changes fairly, transparently and in line with their contracts. The Agricultural Supply Chain Adjudicator (ASCA) is inviting those across the sector to share their views on FDOM24 and to voice any potential concerns around non-compliance and unreasonable behaviour in a short survey. The survey asks about the regulations, the role of the ASCA, and how relationships between producers and purchasers have worked during this challenging period. Follow the attached link to access the survey – The Agricultural Supply Chain Adjudicator: Milk Sector Survey 2026

Changing demand for dairy products

Grahams Family Dairy has completed a £3.5million extension to its Glenfield site in Fife and now exports products to Hong Kong and the Middle East. The demand for cottage cheese has tripled due to social media trends and many supermarkets are struggling to keep the product on the shelf. Once a staple in the 1970s and 1980s, cottage cheese has landed itself a new audience with fitness enthusiasts, more than 21 million tubs were sold across the UK last year; retail experts predict that high protein dairy products could be worth £400 million in the UK market within the next 5 years.

According to Guernsey Dairy, sales of full fat (blue top) milk have increased by 30% since 2019 from 568,000 litres in 2019 to just over 750,000 litres in 2025. By contrast, low fat milk, which still accounts for the majority of our sales, has declined gradually, while skimmed milk has seen a more noticeable reduction, falling around 23% since 2019. Tesco has also reported a large rise in sales of full fat milk +3 mlitres), a rise of more than 100% compared to two years ago. The changes are thought to be linked to some customers, especially younger customers seeking ‘more natural and minimally processed foods.’

Keira Sannachan, Keira.Sannachan @sac.co.uk

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service