Agribusiness News April 2025 – Sheep

31 March 2025Ramadan Progresses

Ramadan ended on the 30th March, with Eid al-Fitr being celebrated the following day to mark the end of the fast. For this celebration, Muslim families tend to visit friends and family to celebrate the end of fasting and invest in large quantities of meat a few days before this. Typically, we see the sheep trade rise throughout Ramadan, with the extra domestic and worldwide demand. however, this year the price has remained rather steady.

The Islamic calendar follows the Lunar calendar, which follows different phases of the moon. This is 11 days shorter than the solar calendar, meaning the dates for Ramadan change every year.

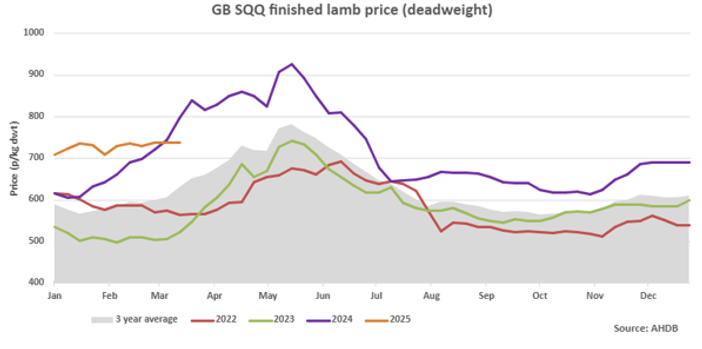

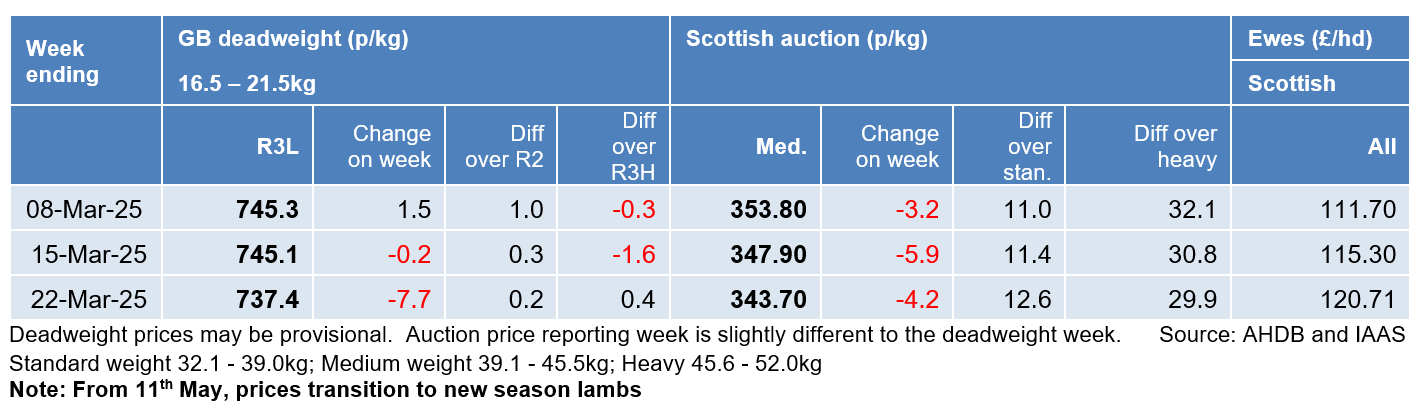

In 2024, the week before Ramadan commenced (w/e 09/03/24) the SQQ was 743.7p/kg DW; this year it was 14p/kg DW back at 729.5p/kg DW (w/e 22/02/25). Looking at week on week prices, for the week ending 15/03/25, the SQQ was 60.1p/kg DW back on the same week last year. The reason for the difference on the year is supply. In 2023, there was a low amount of carry-over of lambs to 2024. However, there has been a larger carry over into 2025, with producers choosing to store lambs longer, aiming for the lucrative spring market. This higher carry over has suppressed the price.

Worldwide

The last month has seen a trade war from Trumps American reign with Mexico, Canada and China. Australia have historically supported the US protein supply with 2024 seeing a total of 394,716 tonnes of beef, 104,210 tonnes of sheep meat and 22,559 tonnes of goat meat, with the USA being Australian meats number one destination. If trade tariffs were imposed on Australia, there could be serious global knock on effects; most concerning for UK would be more product being imported to the UK and Europe.

Meat and Livestock Australia have shared their industry projections for 2025, which shows the national flock decreasing by 5.9 million head (7.4%) to total 73.2 million. The reason for this large decrease is stock ewes which were used to rebuild the flock after droughts in 2020-2022 exiting the flock. However there has been a shift from wool producing breeds e.g. Merino to meat and wool shedding breeds, which has increased productivity, meaning the slaughter numbers won’t decrease as far as the national flock. While the 2025 carcase weights look to remain stable at 24kg; they are set to increase to 24.4kg in 2026, and 24.7kg in 2027.

Live exports are an important market for Australian sheep producers. This will be set to change with live exports by sea being phased out by 1st May 2028. However, there have been disruptions in this area due to the unscheduled maintenance of vessels, and a lack of replacement vessels in this time, which decreased live exports by 33% to 433,078 head in 2024. This disruption looks set to continue for the first half of 2025. World conflict has also had an impact on this market e.g. Israel who import large volumes. The largest markets in 2024 for live exports were Jordan, Kuwait, Saudi Arabia, United Arab Emirates and Israel. The Middle East and North Africa are growing markets, with the Middle East preferring the cheaper Australian product over the higher prices from Romania and Spain, combined with the disease threat from sheep pox, Blue Tongue, etc.

The Australian forecast shows UK as an opportunity, with our reduced national flock and reduced NZ imports due to their flock decrease. In addition, our reducing interest rates (along with US) interest them, as growth is expected in the economy and consumption of protein sources.

Kirsten Williams, kirsten.williams@sac.co.uk 07798617293

Related articles

Rural Business

Sheep

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service