Agribusiness News November 2024 – Cereals

1 November 2024Scottish Harvest Estimate

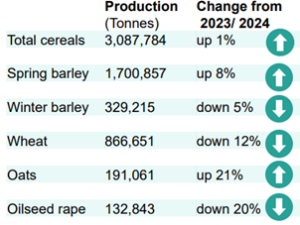

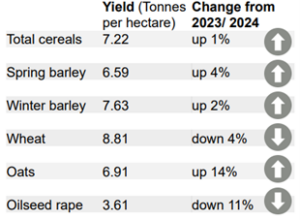

The first estimate of Scotland’s 2024 cereal and oilseed rape harvest has been issued by RESAS (Rural and Environmental Science and Analytical Services, within Scottish Government). Following industry consultation, total cereal production is expected to remain at around 3.1 Mt, just above the ten-year average. Wheat, winter barley and oilseed rape see overall production falls, contrasting with increases in spring barley and oat production. Final results will be published in December and the infographic shown below illustrates the interim estimates of National production and yield per ha.

Figure 1: Scottish cereal production 2024 (tonnes). Source: ScotGov

Figure 2: Scottish cereal production 2024 (t/ha). Source: ScotGov

Similarly, AHDB published the 2024/25 Early Balance Sheets for wheat and barley for the UK. Wheat production, at 11.05 Mt, is down 21% on last year and despite the heaviest opening stocks for over 20 years, home produced availability for 2024/25 will be down 9% requiring an estimated import requirement of 2.63 Mt. A 3% rise in barley production more than offsets declines in opening stocks and imports therefore national availability of barley is expected to increase 1% to 8.49 Mt. Domestic consumption on farm is anticipated to rise by 8% as inclusion in rations looks more favourable to wheat given relative pricing. With H&I (Human & Industrial, i.e. for flour, malting, brewing & distilling) barley consumption set to fall 4%, net domestic consumption is forecast up 4% on 2023/24.

Wheat market remains pressured

Markets are reacting to weather issues across Europe and the Black Sea Region. Russia’s autumn planting campaign was stalled by very dry conditions and consequently 2025’s wheat crop is being projected at 80 Mt (down 1 Mt from the 2024 harvest); this represents a fourth successive fall in output in as many years.

France, the EU-27’s largest producer, has not only seen its smallest wheat crop in 40 years, but is also well behind in its autumn planting campaign for 2025, having experienced persistent wet weather through September. Markets are trying to balance these bullish factors of potentially lower production and stock reductions against the general lack of global demand acting to suppress prices. Currently, Russian and Ukrainian export price trades lower than EU origin grain and this, together with the pace of exports, continue to set the market.

Figure 3: London wheat prices, May 2024-May 2025. Source: ECD, ICE, CME, MGEX, MRCI, DCE

UK malting barley demand is reported lower by 83 Kt (4%) compared to last year and playing its part in stifling premiums. Rapeseed, conversely, sees strong support mostly driven by the fundamentals of supply and demand and the expectation of lower global production this year into next is likely to keep prices supported.

mark.bowsher-gibbs@sac.co.uk 07385 399 513

|

Indicative grain prices week ending 28/10/2024 Source: SAC//United oilseeds/Farmers weekly/AHDB) |

| £ Per Tonne | Basis | Nov '24 | Mar '25 | Nov '25 |

|---|---|---|---|---|

| Wheat | Ex Farm Scotland | 200 | 205 | 201 |

| Feed Barley | Ex Farm Scotland | 170 | 175 | 171 |

| Oats Milling | Ex Farm Scotland | 330 | ||

| Oilseed Rape | Ex Farm Scotland | 402 | 405 | 385 |

| Beans | Ex Farm Scotland | 225 |

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service