Agribusiness News October 2024 – Sheep

30 September 2024Store and breeding sales have continued to hit the headlines, with record breaking prices being made across the country this Autumn. This has been in response not just to the decrease in the global ewe flock, but also to the positivity surrounding the sheep sector with strong prime prices and a growing Muslim population.

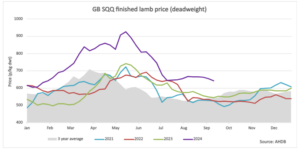

While the prime price has fallen as supply has increased; there are reports of lower carcass weights and leaner lambs, which affect the average. For the week ending 14th September 2024, the SQQ price stood at £6.42/kg, which was 97 pence per kg higher than the same week last year.

Around the Globe

Prices of tradable commodities such as sheep meat, are largely priced depending on supply, demand and world currencies. Beef and Lamb New Zealand recently published their new season outlook. They have outlined that the next lamb crop will be reduced by 5% to 19.2million head. The reduction is largely due to less ewes and a higher level of replacements being retained to rebuild flocks following droughts in 2024. With this smaller lamb crop coming from a large exporting country, it is worth understanding where the rest of the globe is in terms of economics and demand of sheep meat.

China’s economic recovery from the pandemic is taking longer than the rest of the world. With this, the demand for red meat is not as strong as it has been in the past. However, China is still New Zealand’s largest export market, with 37% of lamb and 77% of mutton being imported to China in 2023/24.

America has a growing demand for lamb, with consumption levels increasing, especially in the high value cuts. Demand is increasing in lamb in the younger demographic, as well as their being an increasing Muslim population in the US.

European flocks are decreasing in size, resulting in lower production, and less sheep meat available for domestic consumption.

Australia has been dominating the world lamb production of late. However, their national flock has peaked, with an estimated rise of 11% in the lamb crop between 2023 – 2024. This is now set to decrease by 5% from 27.7 million in 2024 to 26.3 million in 2025 following problems with abattoirs being at capacity and low prices. With this lower production, it is expected prices will rise for the marketing of the 2024 crop which started in September.

With each country having their own challenges, from an economics, supply and slaughter capacity, it is clear to see that the global flock is decreasing, while demand is not. Looking at global prices for September, France and Spain are back on top, with New Zealand and Australia gaining pace in their farm gate price.

| Lamb Prices | Week ending 07/09//24 Euros/kg deadweight |

|---|---|

| France | €9.26 |

| Spain | €8.74 |

| UK | €7.76 |

| Austrailia | €5.07 |

| New Zealand | €4.27 |

Source: BordBia

Kirsten Williams, kirsten.williams@sac.co.uk, 07798617293

Deadweight prices may be provisional. Auction price reporting week is slightly different to the deadweight week. Source: AHDB and IAAS

Standard weight 32.1 – 39.0kg; Medium weight 39.1 – 45.5kg; Heavy 45.6 – 52.0kg

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service