Business and Policy August 2025 – Beef

31 July 2025Sharp decline in beef prices levelling off as beef remains in tight supply

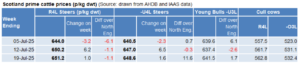

After several weeks of finished price declines – 70p/kg beef drop in 6 weeks – deadweight prime cattle prices in Scotland have been more stable since the week of the Highland show, with price reductions averaging 1p at the end of June and first week of July. While down 11% from their peak, prime cattle still averaged 33% higher than a year earlier at the start of July, at 641.6p/kg/dwt. For week ending 19 July, R4L grades were sitting at 651p/kg (+1p from the previous week). Angus cattle are currently sitting around 660p/kg/dwt.

While a drop in fat price was anticipated over the summer, as consumers holiday abroad and seasonality means beef sales shift towards cheaper products such as burgers in the summer; AHDB recently reported that consumer demand up to mid-June was at its lowest since September 2024. With beef sales rebalancing towards cheaper cuts, processors are struggling to sell steak meat which is causing carcase imbalance issues and contributed to the sharp declines witnessed from the beginning of May.

Beef remains in tight supply, with total cattle throughputs at UK abattoirs down by 4% during the first half of the year. For week ending the 12th of July, UK estimated prime cattle slaughterings were sitting at 30,00 head (down 1,850 head against the same week in 2024) and were significantly below the year-to-date kill – more than 4% lower than the same period in 2024.

Although the beef market looks to be stable for now, sitting at a higher price level compared with summer 2024 prices; reports suggest that prices will start to increase further as low cattle supplies both domestically and globally become a bigger price driver than demand from consumers.

Store Cattle in demand but in short supply

Store cattle prices have remained strong throughout July against sharp declines in finished prices, which will inevitably lead to pressure on prime cattle margins. Although this is not the time of year for major sales of store cattle, those markets which have had store sales have reported a lift in sale averages. Rain easing grazing pressure alongside favourable feed costs including cheap barley has incentivised buyers of store cattle, with forward stores in high demand.

The problem is that, although there is an increase of buyers, there is not an increase in store cattle coming forward. Bluetongue restrictions are also pressuring the store ring – as Scottish buyers can no longer buy stores from England, therefore increasing the competition in Scottish store rings.

Cull cow prices lifting but numbers getting tighter

Cull cow prices have seen an uplift recently, with abattoirs keen to secure supplies for processing beef, where carcass imbalance is less of an issue. Similar to prime cattle prices, cow prices have also seen record highs in 2025, with prices up 38.5% compared to 2024 levels and 51% higher than the 5-year average. Trade for cull cow is sitting around 550-560p/kg/dwt.

Figures from AHDB show cow slaughterings down 12.7% compared to July 2024, highlighting a contracting national herd size is limiting the number of cows coming forward. Are we now reaching a crunch point where available supplies cannot sustain historic kill levels?

Sarah Balfour, sarah.balfour@sac.co.uk

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service