Agribusiness News January 2025 – Milk

1 January 20252024 review: a year of two halves

- Rising prices for butter, cream, SMP and cheddar came on the back of low milk volumes both here and in the EU in the first half of 2024.

- Milk volumes rose in the second half of 2024 stimulated by milk price rises and lower feed costs.

- Milk price has been below the cost of production for much of the year, but margins have been improving.

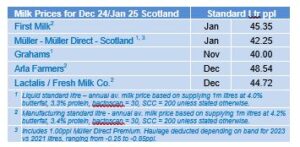

Milk prices were pretty static for the first half of 2024, with the Defra average farm-gate milk price ranging from 38.03ppl to 38.92ppl from January to June. With a poor start to the milk year with lower milk volumes due to a cold, wet spring and a subdued spring flush, the Defra milk price started to head north quickly and reached 45.17ppl in October, just over 8ppl more than 12 months ago. Arla and Lactalis have had 11 monthly milk price increases this year, First Milk with 10 and Muller with 6. None of these processors had a month where their milk price dropped in 2024.

Milk volumes have reflected the atrocious weather conditions in the first half of the year, hampering grass growth and delaying turnout in many areas. Volumes were down and apart from February, monthly GB deliveries from January to July were less than the previous year. AHDB’s December forecast is estimating GB production for 2024/25 to be 12.43 billion litres, 0.9% more than the previous milk year.

As a result, wholesale prices particularly for fats started to head north from April onwards. With the seasonally lower butterfat levels, lower milk volumes and a poor spring flush, butter and cream prices skyrocketed, with butter reaching an all-time high average monthly price of £6,730/t in September. Stocks were very tight and with a cream shortage, butter manufacture took a hit with sales of cream prioritised rather than incurring production costs from churning cream into butter.

Given the rise in milk prices and the easing of feed costs, with soya back over £100/t from 12 months ago, the milk price to feed price ratio has been more favourable and encouraged higher concentrate feeding rates to stimulate production in the second half of the year. In addition, from September onwards, grass growing conditions and grass quality improved, with September and October GB production being higher than the same months in 2023. More Autumn calving cows have also contributed to production increases. At the time of writing, the estimated GB November volume was 4.4% up on November 2023.

For the 2023/24 milk year, the average cost of production was calculated at 45.0ppl by The Dairy Group, with an estimated cost of 44.2ppl for the 2024/25 milk year, leaving a 0.5ppl profit after accounting for family wages. This is well above the Defra average farm-gate milk price from April to September this year. However, interestingly there was nealy a 9ppl difference in cost of production between the top 25% and the average dairy farms.

2025 dairy outlook

Rabobank Research predicts that global milk supply will increase by 0.8% in 2025. With rising milk prices and feed being more affordable it is expected that all seven main exporting regions (New Zealand, Australia, the EU, the US, Uruguay, Brazil and Argentina) will see year-on-year growth in 2025 – this has not been the case since 2020. China’s domestic milk production is expected to decline by 1.5% in 2025, which will likely end their three-year run of falling net imports. Chinese imports are predicted to rise by 2% in 2025 on the back of lower milk supply and improving consumer demand. Globally, demand for dairy products is expected to improve, and with more milk, the dairy markets remain fairly well balanced going forward into 2025. However, as always, the market is sensitive to many factors: geopolitical events, disease and weather will always impact production and trade. Bluetongue in the EU and avian influenza in the US could affect herd numbers and milk output but there is confidence that vaccines will limit production impacts. The new Trump administration could affect markets if new tariffs disrupt the flow of trade and there is the risk of less labour on US farms if the threat of mass deportations are realised.

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service