Business and Policy July 2026 – Milk

2 July 2026Milk production data

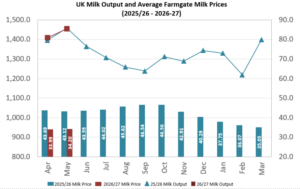

Milk production is declining and the spring flush has well and truly passed. The latest data from AHDB estimates the GB milk volume for May at 1,167m litres, 19m litres less than the previous May. Daily production is currently 35.97m litres for the week ending 20th June, 1.2% less than the previous week and 1.4% less than the same week last year. For the UK, May milk volumes were 1,454m litres, which is 54m litres (3.5%).

Farm-gate prices

The Defra farm-gate milk price for May 2026 was 34.20ppl down 0.15ppl (0.4%) from the April price and 21% lower than 12 months ago. Grahams announced price holds for July, with First Milk and Arla announcing a price increase. The organic milk price is currently around 56ppl.

Milk Prices for June/July 2026 Scotland Standard Ltr ppl

First Milk2 July 31.35

Müller - Müller Direct - Scotland 1, 3 June 34.5

Grahams1 July 34.5

Arla Farmers2 July 37.24

Lactalis / Fresh Milk Co.2 June 31.24

1 Liquid standard litre – annual av. milk price based on supplying 1m litres at 4.0% butterfat, 3.3% protein, bactoscan = 30, SCC = 200 unless stated otherwise.

2 Manufacturing standard litre - annual av. milk price based on supplying 1m litres at 4.2% butterfat, 3.4% protein, bactoscan = 30, SCC = 200 unless stated otherwise.

3 Includes 1.00ppl Müller Direct Premium. Haulage deducted depending on band for 2023 vs 2021 litres, ranging from -0.25 to -0.85ppl.

Dairy commodities & market indicators

This month has brought further challenges for markets, with conditions deteriorating towards the end of the reporting period. Trading has been exceptionally quiet, with high inventories of some commodities weighing on sentiment. While seasonal slowdowns are typical ahead of the European summer holidays, market activity this year has been particularly subdued.

UK milk production has remained below year-ago levels since April, creating some spare processing capacity, although comparisons are against exceptionally high volumes. Meanwhile, strong European milk supplies continue to pressure the wider market, and with substantial product still in storage, any recovery is expected to be gradual.

Skimmed Milk Powder (SMP)

Skimmed Milk Powder eased back from the highs reached last month, bringing to an end the positive start to 2026. The price has corrected to align with more competitive levels in other markets. This has resulted in a decline of £210/tonne, the average price for the period was £2,290.

Mild cheddar

The cheddar market has experienced similar conditions to last month with supply and demand being balanced. Some traders are looking to sell the commodity at cheaper prices which is pulling the overall value down slightly. The average price for the period was £2,890, losing a further £50/tonne.

Bulk cream

Bulk cream was the strongest performing commodity in the period, supported by tightening milk supplies. Average prices increased significantly compared with the previous reporting period, although they have eased off slightly in recent weeks. The premium over EU prices remains too high to encourage trade flows, while demand is also reported to be softening. The average price for the reporting period was £1,387/tonne.

Butter

Butter remained under pressure due to high milk volumes and substantial stocks. Demand was reported to be very limited, with prices coming under further pressure ahead of the summer holidays. Butter prices are now well below cream returns which should discourage production in the short term. Demand remains weak, with market activity reported to be incredibly quiet. As a result, prices continue to decline, falling by a further £90/tonne to £3,240/tonne, the lowest level since July 2021.

There was a very small increase in AMPE and a small fall in MCVE in May. The Milk Market Value indicator reduced by 1.12ppl to 33.60ppl for June. The latest GDT auction on 16th June shows a decline of 2.8% in price when compared to the previous auction, with the average price across all products reaching $3,979/t.

| UK dairy commodity prices (£/tonne) | June 2026 | May 2026 | December 2025 |

|---|---|---|---|

| Butter | 3,240 | 3,330 | 3,710 |

| Skim Milk Powder (SMP) | 2,290 | 2,500 | 1,730 |

| Bulk Cream | 1,387 | 1,220 | 1,312 |

| Mild Cheddar | 2,890 | 2,940 | 2,830 |

| UK milk price equivalents (ppl) | June 2026 | May 2026 | December 2025 |

|---|---|---|---|

| AMPE | 32.93 | 35.54 | 29.9 |

| MCVE | 33.77 | 34.52 | 31.5 |

© AHDB [2025]. All rights reserved.

Rabobank Global Outlook

Rabobank has stated in their quarterly update that global milk production is slowing after a period of rapid expansion, signalling a return to a better balance between supply and demand. The bank has forecast that milk production will finish quarter two 1.5% higher than last year, before flattening in quarter three and falling by 1.6% in quarter four. The slowdown follows four consecutive quarters of strong growth, with annual production peaking at 5.2% at the end of 2025, which is one of the largest increases on record. RaboResearch senior dairy analyst Michael Harvey said higher feed and input costs, tighter farm margins and uncertain milk prices are expected to curb production. Weather risks, including a potential strong El Niño, and ongoing geopolitical tensions could also affect global dairy markets.

Fore-milking can increase mastitis detection

Research conducted on 80 dairy farms in Ireland found that routine fore-stripping increased mastitis detection by up to 146%, suggesting many cases are being missed. There were 40 control farms that continued standard milking practices, while 40 did a week of fore-stripping three times across the 13-month trial window. The intervention farms were provided with a strip cup, which aids the visible detection of clots or other abnormalities in the milk. PhD student Rachael Millar said fore-stripping should be used year-round, not just during particular times of the year, as earlier detection can improve treatment success and help reduce the spread of infection. The study found environmental bacteria were the main cause of clinical mastitis, with Streptococcus uberis the most common pathogen, followed by E. coli and Staphylococcus aureus. Detection increased during each intervention period, rising by 16% in spring, 119% in summer and 146% in winter, highlighting the value of regular fore-stripping throughout the year. The preliminary findings were presented at the British Mastitis Conference in June 2026.

Keira Sannachan, Keira.Sannachan@sac.co.uk

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service