Business and Policy June 2026 – Milk

1 June 2026Milk production data

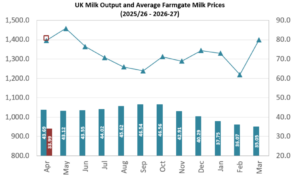

GB production for the year ending 31st March 2026 is estimated to have reached 13.02 billion litres, a significant increase of 5.0% when compared to the previous season. This is the highest volume recorded for a milk-year. The latest data from AHDB estimates the GB milk volume for April at 1,136 million litres, 5m litres more than the previous April. Daily production is currently 38.12m litres for the week ending 16th May, 0.8% less than the previous week and 0.5% less than the same week last year. For the UK, April production was 1,400m litres, which is 4m litres more than April 2025. Despite price cuts since late autumn, milk volumes have been slow to reduce as the milk to feed price ratio remained in the expansion zone.

Ground and forage conditions have been supporting milk from grass production; grazing conditions have seen an improvement against this time last year when many areas were experiencing drought. AHDB has also reported that a plateau of daily GB milk deliveries observed at the end of April, highlights that we have most likely now passed the peak of the spring flush. This is unseasonably early and typically occurs during the first few weeks of May.

![]()

Farm-gate prices

The Defra farm-gate milk price for April 2026 was 33.99ppl down 0.78ppl (2.2%) from the March price and 22% lower than 12 months ago. Grahams, Muller and First Milk announced price holds for June. The organic milk price is currently around 56ppl.

| Milk Prices for June 2026 - Scotland | Standard Ltr ppl | ||

|---|---|---|---|

| First Milk2 | June | 30.75 | |

| Müller - Müller Direct - Scotland 1, 3 | June | 34.5 | |

| Grahams1 | June | 34.5 | |

| Arla Farmers2 | June | 35.83 | |

| Lactalis / Fresh Milk Co.2 | June | 32.79 | |

| 1 | Liquid standard litre – annual av. milk price based on supplying 1m litres at 4.0% butterfat, 3.3% protein, bactoscan = 30, SCC = 200 unless stated otherwise. | ||

| 2 | Manufacturing standard litre - annual av. milk price based on supplying 1m litres at 4.2% butterfat, 3.4% protein, bactoscan = 30, SCC = 200 unless stated otherwise. | ||

| 3 | Includes 1.00ppl Müller Direct Premium. Haulage deducted depending on band for 2023 vs 2021 litres, ranging from -0.25 to -0.85ppl. | ||

Dairy commodities & market indicators

Milk supplies are beginning to come under control; there are signs that the markets are slightly less pressured, but there is still a long road to recovery with so much product in store.

Skimmed Milk Powder (SMP)

Skimmed milk powder remains the strongest performing commodity relative to fats. Prices rose by £140/t to £2,500/t, prices have not been seen at these levels since November 2022. Demand for protein remains strong, with prices remaining very competitive, especially when compared to the United States. This level of demand would be even higher if it wasn’t for export difficulties due to the ongoing conflicts.

Mild Cheddar

There is a lack of excitement in the cheddar market, with quiet demand and a fairly balanced market. Cheddar prices are unsurprisingly back as a result. The average price for mild cheddar was £2,940/t, this is 1% lower than the previous period.

Bulk Cream

There was some movement in prices through the month, from a low point in the 1.00’s up to the low 1.30’s at the end of the period. The average price for the month was £1,220/t which is similar to the previous month, despite some volatile movement in between reports. As we have passed the peak of the flush, the tightening milk supply will offer support for bulk cream prices. Prices remain at around half the value of this time last year.

Butter

Due to reportedly high volumes in store and high milk volumes, butter has continued to struggle over the past month. The market is reliant on demand as the churns are working at capacity with nowhere for the product to go. Cream is undervalued when compared to butter, so there is scope to make money if there is capacity to churn and store, which keeps pressure on the price. The price of butter moved down by £210/t to £3,330/t, this masks some fluctuations during the month, and sentiment is becoming increasingly positive within the last week.

As a result, there was marginal change in the AMPE and MCVE. The Milk Market Value indicator reduced by 0.18ppl to 34.73ppl for May. The latest GDT auction on 19th May shows a slight recovery of 0.6% in price when compared to the previous auction, with the average price across all products reaching $4,198/t.

| UK dairy commodity prices (£/tonne) | May 2026 | April 2026 | November 2025 |

|---|---|---|---|

| Butter | 3,330 | 3,540 | 4,290 |

| Skim Milk Powder (SMP) | 2,500 | 2,360 | 1,800 |

| Bulk Cream | 1,220 | 1,238 | 1,752 |

| Mild Cheddar | 2,940 | 2,980 | 2,960 |

| UK milk price equivalents (ppl) | May 2026 | April 2026 | November 2025 |

|---|---|---|---|

| AMPE | 35.54 | 35.25 | 33.6 |

| MCVE | 34.52 | 34.82 | 33.0 |

Nestlé & First Milk launch Young Dairy Leaders programme

A new initiative aimed at supporting the next generation of dairy farmers has been launched by Nestlé and First Milk. Developed in partnership with 8point9 Training and Education, the programme offers practical hands-on learning, tailored to the realities of modern dairy farming. Running throughout 2026, Young Dairy Leaders is open to First Milk members seeking relevant development opportunities to strengthen both business performance and personal growth, while building a strong sense of community.

The influence of genetics on lowering emissions

Research commissioned by AHDB and carried out by Promar International has found that targeted breeding could help dairy farms cut carbon emissions by up to 16% over five years. The study focused on AHDB’s EnviroCow index, which ranks cows based on environmental efficiency traits. Herds using higher ranking bulls achieved emissions reductions of between 8.5% and 16%, highlighting the growing role genetics can play in improving sustainability. Researchers also found strong links between lower emissions and other breeding indexes, particularly the Profitable Lifetime Index (£PLI). Farmers are encouraged to continue prioritising breeding-for-profit indexes such as £PLI, while also seeking opportunities to improve EnviroCow scores where appropriate. Breeding decisions should take a balanced approach, considering a range of important traits rather than focusing solely on emissions reduction.

Keira Sannachan, Keira.Sannachan @sac.co.uk

Sign up to the FAS newsletter

Receive updates on news, events and publications from Scotland’s Farm Advisory Service